Will the banking system collapse in 2024?

Will the banking system collapse in 2024?

As we venture deeper into 2024, the echoes of the past year's tumultuous events in the financial sector still resonate, shaping the current economic narrative. The sudden and startling collapse of Silicon Valley Bank, along with two other significant financial institutions in early 2023, has cast a long shadow over the banking industry. This incident, more than just a wake-up call, has thrust the intricate challenges of interest rate risk management into the limelight.

Investors and regulators, now with heightened vigilance, are closely scrutinizing the risks pervading the banking sector. These risks are not new; they range from cyber threats and fraud to shifts in depositor behavior, seeking higher returns, and the lingering pandemic effects on investment and loan portfolios.

However, the recent events have not only underscored these risks but also revealed their growing complexity and interconnected nature. This article aims to dissect these concerns, propelled by recent financial upheavals and market instabilities.

Current Economic Landscape

The global economic scenario presents a mixed bag of challenges and opportunities for the banking sector in 2024. Key indicators such as interest rate trends, inflation, and global debt levels are exerting significant pressure. The International Monetary Fund (IMF) and World Bank have repeatedly warned of these challenges, emphasizing the need for robust financial buffers.

Global Economic Slowdown: The global economy is expecting a slowdown in 2024, creating a challenging environment for banks. This slowdown is characterized by divergent economic conditions across different regions. Advanced economies like the United States, Euro area, Japan, the United Kingdom, and Canada are projected to see modest growth, while emerging economies, particularly India, are expected to witness higher growth rates.

Compounding these challenges is the significant impact of rising interest rates on banks' bond portfolios. A recent study reveals a striking $2.2 trillion discrepancy between the market and book values of U.S. banking assets, underscoring the financial system's vulnerability. Furthermore, long-term bond yields have surged to levels not seen since 2007, intensifying the pressure as the Federal Reserve continues to hike interest rates.

The signs of a shifting credit cycle are also evident in the $1.5 trillion highly leveraged loan market, where defaults are escalating. Goldman Sachs reports defaults totaling $24.5 billion, marking this as potentially the third worst year for loan defaults in history. Similar trends are observed in the auto loan and credit card sectors, indicating broader financial stresses. This complex economic landscape, marked by regional disparities and internal banking sector pressures, sets a challenging course for banks navigating through 2024.

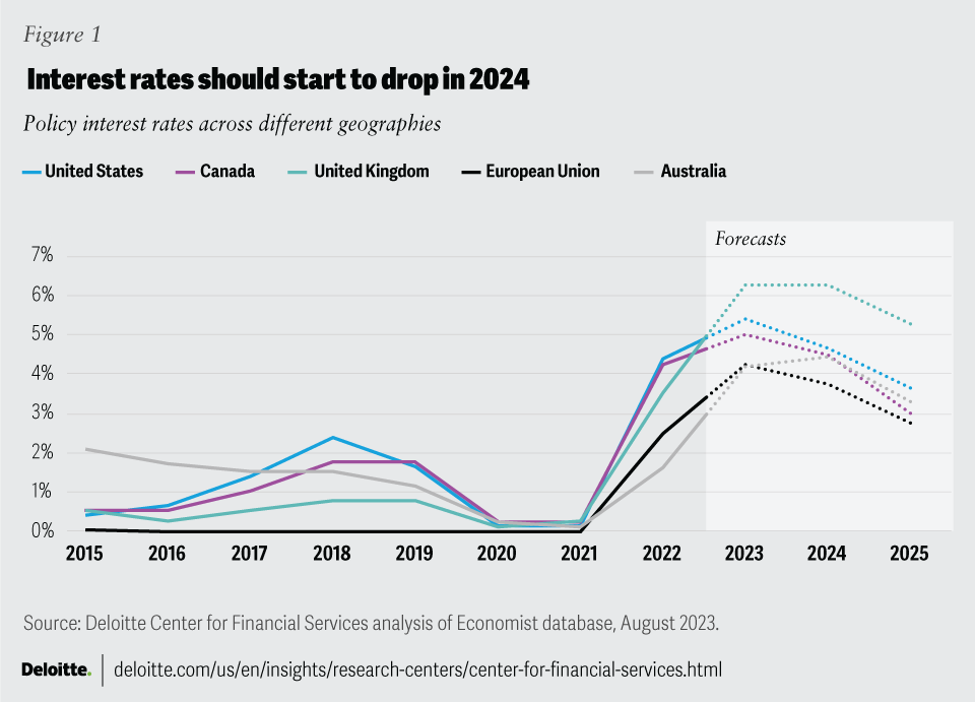

High Interest Rates and Changing Monetary Policies: Central banks, including the U.S. Federal Reserve and the European Central Bank, are adjusting their monetary policies to combat inflation and stabilize economies.

The Federal Reserve, for instance, is expected to maintain elevated interest rates for a significant part of 2024 before potentially lowering them in the latter half of the year. These high interest rates have increased the cost of borrowing and impacted bank margins, particularly for regional banks.

Impact on Loans and Consumer Spending: There is an expectation of modest loan growth due to the macroeconomic conditions and high borrowing costs. Consumer spending is also likely to slow down compared to the pace in 2023, influenced by factors like diminished savings and plateauing wage gains. However, household balance sheets remain healthy, and tight labor markets continue to support employment and income levels.

Commercial Real Estate Concerns: The commercial real estate sector, particularly in the U.S., is facing challenges with mortgage origination and refinancing, given the higher interest rates and changing consumer behaviors. This could have significant implications for banks with exposure to this sector.

Regulatory Changes

Banks are facing heightened regulatory and supervisory focus in 2024. This includes increased attention to liquidity regulation, resolution, and recovery strategies. In the wake of recent bank failure events, banks are now compelled to reassess risks of contagion and develop more sophisticated approaches to stress testing, including non-financial risks. This is something that we did not see leading up to the 2008 financial crisis.

This situation requires banks to proactively engage with regulators and fortify their operational resilience frameworks, especially in light of advancing digitization and AI adoption.

Capital Requirements and Industry Pushback:

One of the contentious areas is the imposition of stringent new capital reporting requirements under section 1071 of the Dodd-Frank Act. Banks are concerned about being overwhelmed with data, which is likely to lead to compliance issues. According to Peter Dugas, the executive director at Capco “The challenge is the compliance with the rule due to the complexity and the overall data collection. People have completely underestimated the complexity of this.” While the new rules have the potential to help both the investors and clients, banks will have to adjust and take the pressure of increased compliance procedures.

Challenges with Fintech Partnerships:

The relationship between banks and fintech companies is undergoing a transformation. Banks are becoming more selective in their partnerships with fintech firms, and the cost of managing risks in these collaborations is expected to increase. This change is partly driven by greater regulatory focus on banking-as-a-service models. Fintechs may need to bear a more significant portion of risk management costs, potentially impacting their operational models and strategies.

Basel III Endgame

The Basel III "endgame" proposal, introduced by banking regulators and detailed in an EY report from September, is set to significantly change how large banks, specifically those with assets exceeding $100 billion, manage and calculate risk-based regulatory capital. This new proposal is expected to lead to an increase in the risk-weighted assets of these banks. Additionally, it will necessitate smaller banks to improve their risk data, technology capabilities, and controls to meet these new requirements. Essentially, this means that banks will need to adjust their approach to managing financial risks and their capital, aligning with the evolving regulatory landscape.

Technological Advancements

In 2024, the banking sector is set to undergo significant transformation due to technological advancements, leading to improved operational efficiency and reshaped customer experiences. Key highlights of these changes include:

Generative AI: This technology is revolutionizing trading operations by analyzing large volumes of textual data for insights, thus enhancing speed and volume in trading activities. The use of generative AI in banking is growing rapidly.

Embedded Finance: This emerging trend integrates banking services into non-financial platforms. It's driven by payment processing through embedded channels and models like Buy Now, Pay Later (BNPL) plans, significantly contributing to banking revenue.

Open Banking: This trend involves sharing customer data securely via APIs, promoting collaborations between banks and non-banking financial companies. It's supported by technologies like blockchain and AI, leading to more innovative financial solutions.

Hyper-Personalization: Banks are using real-time data and AI for personalized customer service, tailoring financial recommendations and services to individual needs.

Cybersecurity: With the adoption of these advanced technologies, banks face increased cybersecurity challenges and are investing in robust security measures to protect their systems and customer data.

These technological advancements are not only enhancing the way banks operate but also transforming how they interact with customers, necessitating ongoing adaptations in their strategies and operations.

Historical Context

Historically, banking crises have been addressed with decisive policy measures, as seen during the 2008 financial crisis where actions by central banks and governments helped prevent a total economic collapse. The potential impact of a banking collapse is extensive, affecting personal savings, corporate investments, households, and small to medium-sized enterprises (SMEs), potentially leading to significant economic distress.

Key responses to such crises include:

Monetary Policies: Central banks have typically employed strategies such as lowering interest rates and providing liquidity to stabilize the financial system.

Fiscal Interventions: Governments have often increased spending, guaranteed deposits, and invested in key financial institutions to bolster confidence and prevent further collapses.

Regulatory Reforms: Post-crisis, focus has been on enhancing the regulatory framework, such as increasing capital requirements for banks and introducing liquidity standards.

Effective mitigation of banking crises demands coordinated efforts from monetary and fiscal authorities, including clear public communication. The approach to managing these crises draws heavily from lessons learned in past events, particularly the 2007/2008 global financial crisis. The emphasis is on proactive and comprehensive strategies that include both monetary and fiscal tools, as well as regulatory changes, to protect the economy from the consequences of banking collapses.

Conclusion

In light of these varied factors, it appears that the fear of a banking collapse in 2024, while rooted in legitimate concerns, might lean towards being somewhat exaggerated. The banking sector, albeit facing significant challenges, is underpinned by stronger regulatory frameworks, technological resilience, and a global economic environment that is slowly stabilizing. The key for stakeholders, from regulators to banks themselves, lies in vigilance, strategic adaptation, and proactive risk management to navigate the current complexities.

In conclusion, while caution and preparedness are warranted, the collective learnings from past crises, coupled with ongoing regulatory and technological advancements, suggest that the banking sector is better equipped to handle the challenges it faces in 2024. The likelihood of a systemic collapse, therefore, while not entirely dismissible, seems to be more a matter of concern than a looming reality.