Why is copper so important to China?

Why is Copper so important to China?

China, the world's second-largest economy, has been on a mission to transform its energy sector and reduce greenhouse gas emissions. As the global demand for renewable energy sources grows, the need for copper has become increasingly important for China, making it essential for the country to develop its renewable energy infrastructure.

In this article, we will explore the significance of copper to China's green ambitions and its role in achieving net-zero carbon emissions by 2050.

China's Copper Demand: Driven by the Property Sector and Green Energy Transition

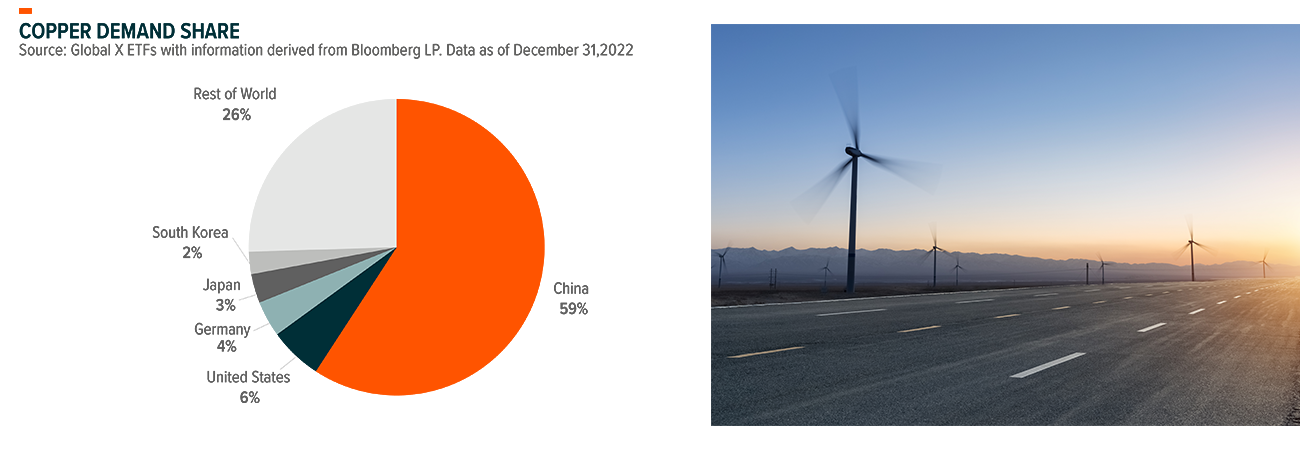

In 2022, China's total copper demand increased by 1.4%, and this year it is projected to grow by 3.2%, amounting to nearly 16.13 million metric tonnes. As the largest consumer of copper, accounting for 59% of the global copper demand, China is going to have a considerable impact on driving this demand.

Source: GlobalXEtfs

At the heart of China's copper consumption lies its building and construction sector, accounting for approximately 30% of total copper end-use. The performance of the Chinese construction sector impacts copper prices quite significantly which is why the recovery of China's property sector from COVID-induced slowdowns is crucial in determining future copper demand.

In November 2022, the China Banking and Insurance Regulatory Commission (CBIRC) introduced a package with 16 steps to support the property sector, including lifting a ban on equity refinancing for developers and permitting private placements for various purposes. This led to the allocation of new loan lines totalling $162 billion from China's leading banks, providing a substantial and synchronized injection of liquidity into the Chinese real estate market. This comprehensive plan should help bolster the property sector, positively influencing copper demand in the building and construction industry.

Copper and Lithium: The New Oil in China's Green Energy Revolution

China's booming property sector recovery, coupled with its transition to green energy, plays a pivotal role in driving the nation's copper demand. As part of China's commitment to achieving net-zero carbon emissions by 2060, the country is heavily investing in renewable energy sources such as solar, wind, and electric vehicles – all of which necessitate significant amounts of copper.

Henry Salisbury, a Research Analyst at Wood Mackenzie, explains that wind power is the most copper-intensive form of energy production. Over the next decade, it is expected to consume the largest amount of copper in the sector.

For instance, the average 3.6MW wind turbine, capable of powering over 3,300 households, contains nearly 29 tonnes of copper. A recent analysis by Wood Mackenzie estimates that between 2018 and 2028, more than 650 GW of new onshore and 130 GW of new offshore wind capacity will be installed. This massive expansion is expected to consume over 5.5 million tonnes of copper, further emphasizing the importance of copper in China's pursuit of a sustainable future.

China is projected to experience the most significant growth in new onshore capacity, consuming an average of 110 thousand tonnes per annum (ktpa) of copper through 2028. The United States follows, with an average consumption of 35 ktpa of copper each year until 2028. Alongside copper, the green energy revolution also requires other crucial resources, such as lithium, which is essential for battery storage solutions. Lithium-ion batteries have taken centre stage in this transition due to their high energy density, long cycle life, and relatively low self-discharge, making them ideal for electric vehicles (EVs) and renewable energy storage systems.

Copper is also an essential component of electric vehicle batteries and charging infrastructure. According to a study by the Copper Development Association (CDA), a typical electric vehicle contains about 183 pounds (83 kilograms) of copper, compared to 18-49 pounds (8-22 kilograms) in a conventional internal combustion engine vehicle.

Similarly, the global demand for lithium batteries is anticipated to increase by over five times by 2030, according to the public-private alliance Li-Bridge. This makes copper and lithium complementary as far as electric vehicles are concerned.

The transition from oil to lithium batteries for electric vehicles (EVs) has led many industry experts, including Goldman Sachs and Elon Musk, to refer to lithium and copper as the new oil. With China being the largest market for EVs, it is no surprise that the demand for these two metals is skyrocketing.

As China accelerates its shift towards sustainable power generation and transportation, the need for these metals will continue to grow exponentially. Copper, in particular, will be crucial for constructing renewable energy infrastructure connecting power grids, and manufacturing electric vehicle components.

Supply Chain Challenges and Price Impacts

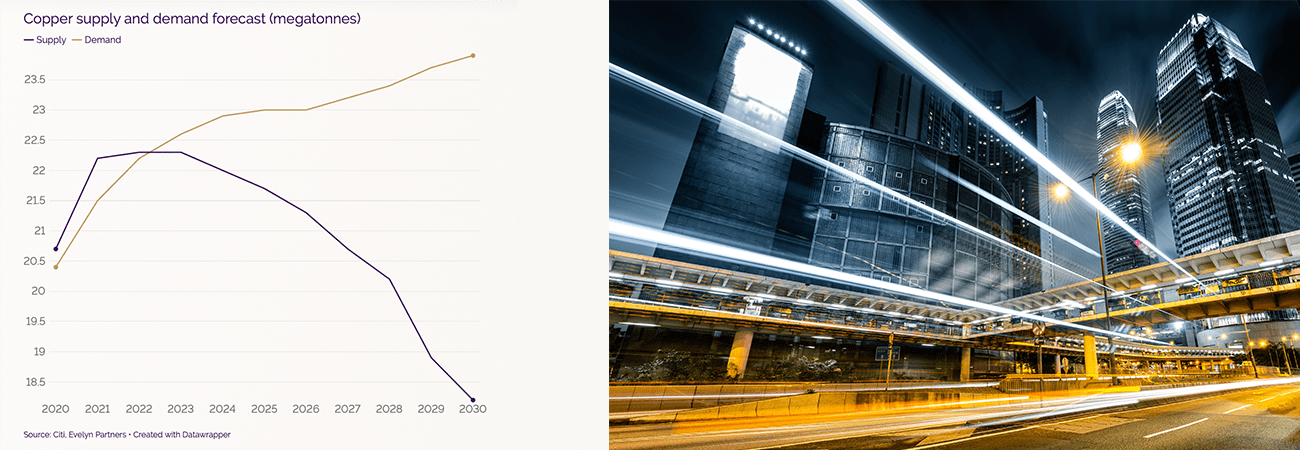

According to McKinsey, the global copper demand is expected to reach 36.6 million metric tonnes by 2031 and the current supply projections put the global supply of copper in 2031 around 30.1 million metric tonnes. This means that there is going to be at least a 6.5 million metric tonne shortfall in supply.

Source: Evelyn

The growing demand for copper in China could lead to supply chain challenges and price impacts. As the demand for copper outpaces the global supply, prices are expected to rise significantly.

The possibility of an increase in copper supply in 2023 due to new projects should be considered alongside the risks of disruptions, especially in important production areas like Central and South America. Chile and Peru, which together provide nearly 40% of the world's copper supply, have faced recent production issues. These problems make it more likely that there could be a shortage of copper in the coming years, which might cause prices to go up. Other challenges in increasing copper production include getting land, connecting to power grids, and dealing with water scarcity in dry areas since copper extraction requires a lot of water.

Low copper supplies in the United States and Europe, along with production issues in South and Central America, create the impression that the copper market may soon face a shortage. If China keeps demanding more copper, Goldman Sachs believes the world could run out of available copper inventory by the third quarter of this year, which would increase the chance of a price surge as traders try to restock.

In fact, according to Bank of America copper prices could reach as high as $20,000 per metric ton by 2025, from the current price of $8,112 per metric tonne.

This surge in demand will likely put pressure on mining companies to increase production, but environmental concerns and the lengthy process of opening new mines could result in supply bottlenecks. These constraints may further exacerbate the supply-demand imbalance and drive copper prices even higher.

Investor Takeaway: Capitalizing on Copper: Embracing Supply Shortages as Investment Opportunities

As China continues to prioritize its green energy transition and strives to achieve net-zero carbon emissions by 2060, the demand for copper is set to surge. Copper plays a critical role in renewable energy infrastructure, electric vehicle manufacturing, and battery storage solutions, presenting a unique investment opportunity for those looking to capitalize on this growing market.

The increasing copper demand is expected to outpace the global supply, leading to supply chain challenges and price impacts. This scenario presents an opportunity for investors to go long on copper, as supply shortages could drive prices higher, potentially generating significant profits. In fact, some analysts predict that copper prices could reach as high as $20,000 per metric ton by 2025.

Investors seeking to benefit from the rising copper demand in China's green energy market should closely monitor the supply-demand dynamics and potential bottlenecks in the copper market. By staying informed and strategically positioning their investments, investors can potentially reap significant rewards from China's ambitious pursuit of a sustainable future.