Which precious metals are good investments in 2026?

Which precious metals are good investments in 2026?

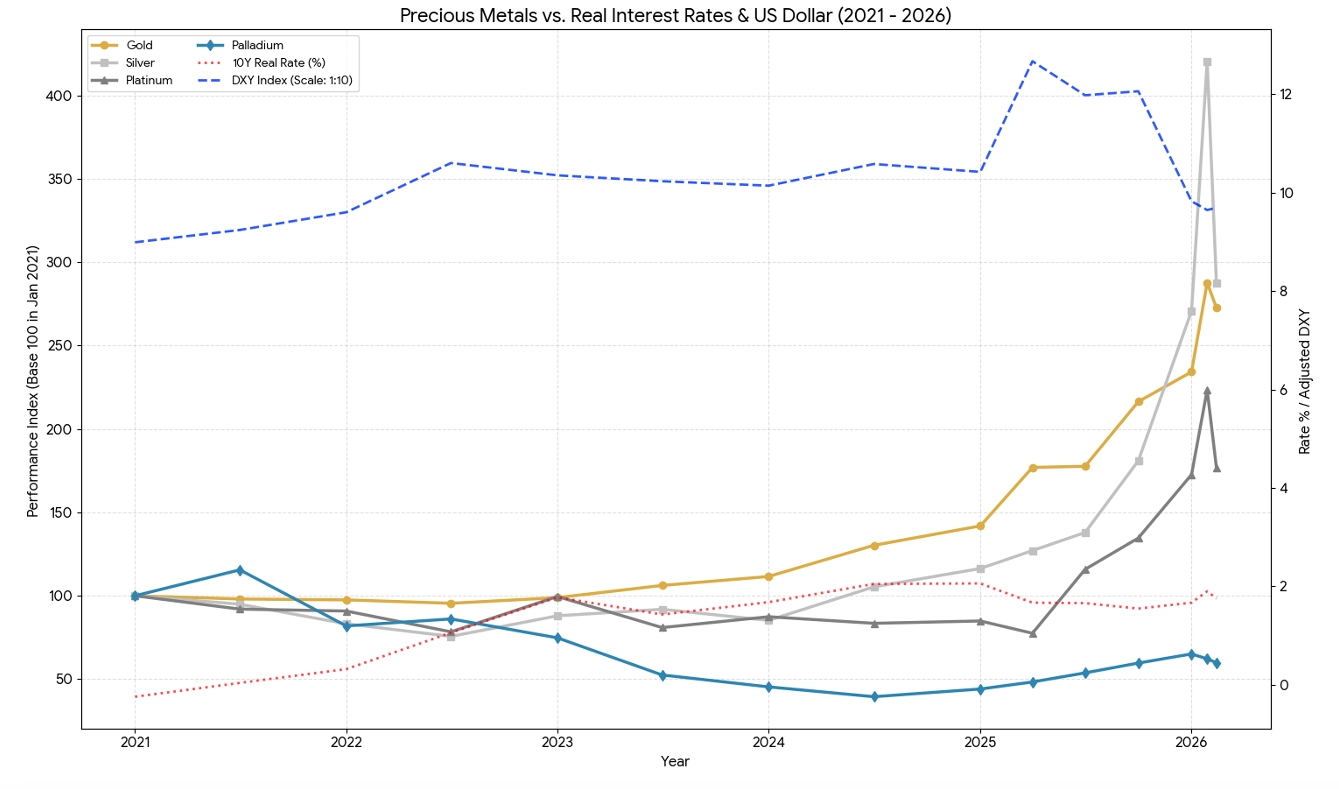

Precious metals are delivering their strongest performance in decades. Gold shattered records above $5,000 per ounce after gaining 65% in 2025, its best year since 1979. Silver briefly topped $120 before a violent 50% correction. Platinum more than doubled. This is not speculative froth. The rally is rooted in structural forces that major investment banks expect to persist.

Gold at $5,000: Structural Repricing, Not a Bubble

Gold is the anchor of any precious metals allocation in 2026. After setting 53 new all-time highs during 2025, gold entered February trading near $5,000 per ounce. The metal surged 13.3% in January alone before a sharp 9% single-day selloff triggered by the nomination of Kevin Warsh as the next Federal Reserve Chair. It recovered within days, retesting $5,000 by early February.

Institutional forecasts for 2026 range from $5,000 to $6,300 per ounce.

- J.P. Morgan raised its year-end target to $6,300, up from $5,055.

- Wells Fargo projects $6,100–$6,300.

- UBS targets $6,200 with an upside scenario of $7,200.

- Deutsche Bank's Head of Metals Research reiterated his $6,000 target, citing "structural demand rather than short-term panic."

- Goldman Sachs sits at $5,400.

The following three structural forces underpin these forecasts.

First, central bank buying has reshaped the market. Central banks purchased 863 tonnes of gold in 2025, the fourth-largest annual expansion on record, led by Poland (102 tonnes), Kazakhstan (57 tonnes), and Brazil (43 tonnes). The World Gold Council's 2025 survey found that 95% of central bankers expect global gold reserves to increase, and 43% plan to increase their own holdings, the highest since the survey began.

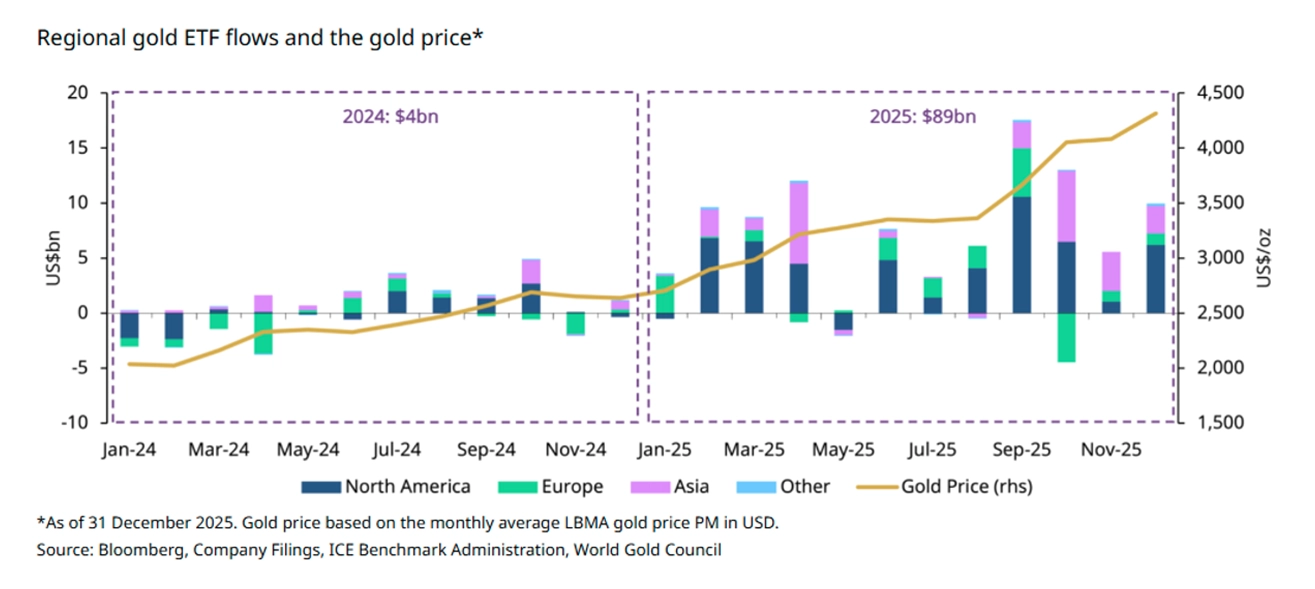

Second, investment demand hit records with global gold ETFs attracting $89 billion in 2025, with holdings growing by 801 tonnes. North American funds alone saw $51 billion in inflows. Even during the January 30 selloff, leading U.S. gold ETFs did not report outflows.

Third, fiscal deterioration provides a long-term floor. U.S. national debt exceeds $38 trillion, with the Congressional Budget Office projecting a fiscal 2026 deficit of $1.85 trillion. Annual interest payments are projected to reach $2.14 trillion by 2036.

J.P. Morgan projects combined investor and central bank demand averaging roughly 585 tonnes per quarter. Natasha Kaneva, the bank's Head of Global Commodities Strategy, stated: "We expect gold demand to push prices toward $5,000/oz by year-end 2026", a target gold has already exceeded.

Gold remains the highest-conviction precious metals investment for 2026. Structural demand from central banks, ETF investors, and fiscal hedging creates a durable floor. The risk is not that the bull case is wrong, but that investors buying at $5,000 must accept that much of the easy upside has already been captured.

Silver's Explosive Rally: Highest Upside, Highest Risk

Silver gained approximately 130–147% in 2025, roughly double gold's return. It briefly breached $112 per ounce in late January before a stunning collapse. The CME hiked margin requirements, triggering what RJO Futures called a "seven sigma event." Silver plunged nearly 50% in the days before stabilizing around $80–$85 in early February.

This volatility is silver's defining feature. Yet the fundamental case for 2026 is arguably stronger than for any other precious metal because it sits at the intersection of monetary demand and industrial necessity.

Industrial consumption now accounts for roughly 58% of silver demand. Solar photovoltaics consumed 257 million ounces of silver in 2024, up 31% year-over-year. The technology shift to TOPCon and SHJ cells uses 1.5x to 2x more silver per gigawatt. Electric vehicles use 67–79% more silver than internal combustion engines, and AI data center servers require 2–3 times as much silver as traditional equipment.

The supply picture is structurally constrained. The silver market has posted deficits for five consecutive years (2021–2025) with a cumulative shortfall of roughly 820 million ounces, equivalent to an entire year of mine production. The Silver Institute projects a sixth consecutive deficit of approximately 67 million ounces in 2026. Mine production peaked in 2016 and has declined since. Over 70% of silver is produced as a byproduct of other mining, meaning supply cannot respond quickly to price signals.

Analyst forecasts reflect both enthusiasm and uncertainty.

- Goldman Sachs projects an average of $85–$100/oz for silver, calling it the "primary strategic metal of the green transition".

- J.P. Morgan forecasts an average of $81 with a high of $85 in Q4, noting this would be more than double its 2025 average.

- UBS sees $100 by March, then $85 year-end.

- Bank of America outlined bull case scenarios ranging to $135–$309.

The gold-to-silver ratio has compressed from over 100:1 in April 2025 to approximately 61:1, after briefly dipping below 50:1 during January's spike. The long-term median sits around 50–60:1.

The key risks for silver are thrift and substitution. The Silver Institute warned that "ongoing thrifting and substitution away from silver will result in falling silver PV demand" even as solar installations rise. Silver-coated copper powder already reduces consumption by 30–50%.

Silver offers the highest potential returns but demands the strongest tolerance for risk. Dollar-cost averaging is essential given the volatility.

Platinum's Deficit Story vs. Palladium's Identity Crisis

Platinum surged approximately 127% in 2025 and hit an all-time high of $2,431 on January 14, 2026, before pulling back to around $2,100–$2,200. The metal is in its third consecutive annual supply deficit, with the World Platinum Investment Council estimating a 692,000-ounce shortfall in 2025, roughly 9% of annual demand.

Bank of America raised its 2026 target to $2,450 per ounce, calling for platinum to "continue outperforming palladium, underpinned by persistent market deficits." The hydrogen economy represents platinum's most exciting long-term catalyst. Platinum is the critical catalyst in PEM fuel cells and electrolyzers. The WPIC projects that hydrogen-related applications will account for 11% of total platinum demand by 2030, up from approximately 200,000 ounces today.

South Africa produces 70–80% of the global platinum supply, constrained by chronic underinvestment, power outages, and declining ore grades.

Palladium rallied 83–91% in 2025 but remains far below its March 2022 all-time high of $3,425. Over 80% of palladium demand comes from automotive catalytic converters for gasoline engines, making it uniquely exposed to the EV transition. The most immediate bullish catalyst is geopolitical: Russia produces approximately 40% of global supply, and potential tariffs could send prices sharply higher.

Five Forces Powering Metals and the One That Could Stop Them

The Fed cut rates to 3.50–3.75% by December 2025, with markets pricing in two to three additional cuts in 2026. The Dollar Index has fallen approximately 9% over the past 12 months to around 97. Goldman Sachs projects DXY retreating to the 98–100 range by year-end 2026.

BRICS nations now conduct over 90% of trade among Russia, India, and China without dollars, and a gold-backed settlement tool called the "BRICS Unit" launched a pilot in October 2025.

Geopolitical instability sustains safe-haven demand. The Russia-Ukraine war continues, Middle East tensions persist, and U.S.-China relations remain strained. The Council on Foreign Relations rates a Taiwan Strait crisis as having an "even chance of occurring in 2026".

The one force that could reverse the rally: a meaningful rise in real interest rates. If inflation cools faster than expected while the Fed pauses or reverses course, positive real rates would increase the opportunity cost of holding non-yielding metals.

Investor Takeaway

The precious metals bull market is driven by factors including de-dollarization, fiscal deterioration, central bank diversification, and green industrial demand. These factors are unlikely to reverse quickly.

Gold remains the highest-conviction allocation. Silver offers the greatest upside for investors who can tolerate volatility. Platinum is the most underappreciated metal with a compelling deficit story and a hydrogen catalyst.

The critical insight for 2026 is that the easy money has likely been made. After gains of 65–147% in a single year, forward returns will be more modest and volatile. The institutional consensus of $5,000–$6,300 gold implies 0–25% upside from current levels. This is attractive but not transformational.

The strongest approach is not to chase metals higher but to build a disciplined, diversified allocation as a permanent portfolio hedge. Dollar-cost average into positions, hold ETFs in tax-advantaged accounts, and rebalance regularly. The structural forces behind this bull market are generational in nature and will outlast any single year's price action.