What does the slump in EV demand mean?

What Does the Slump in EV Demand Mean?

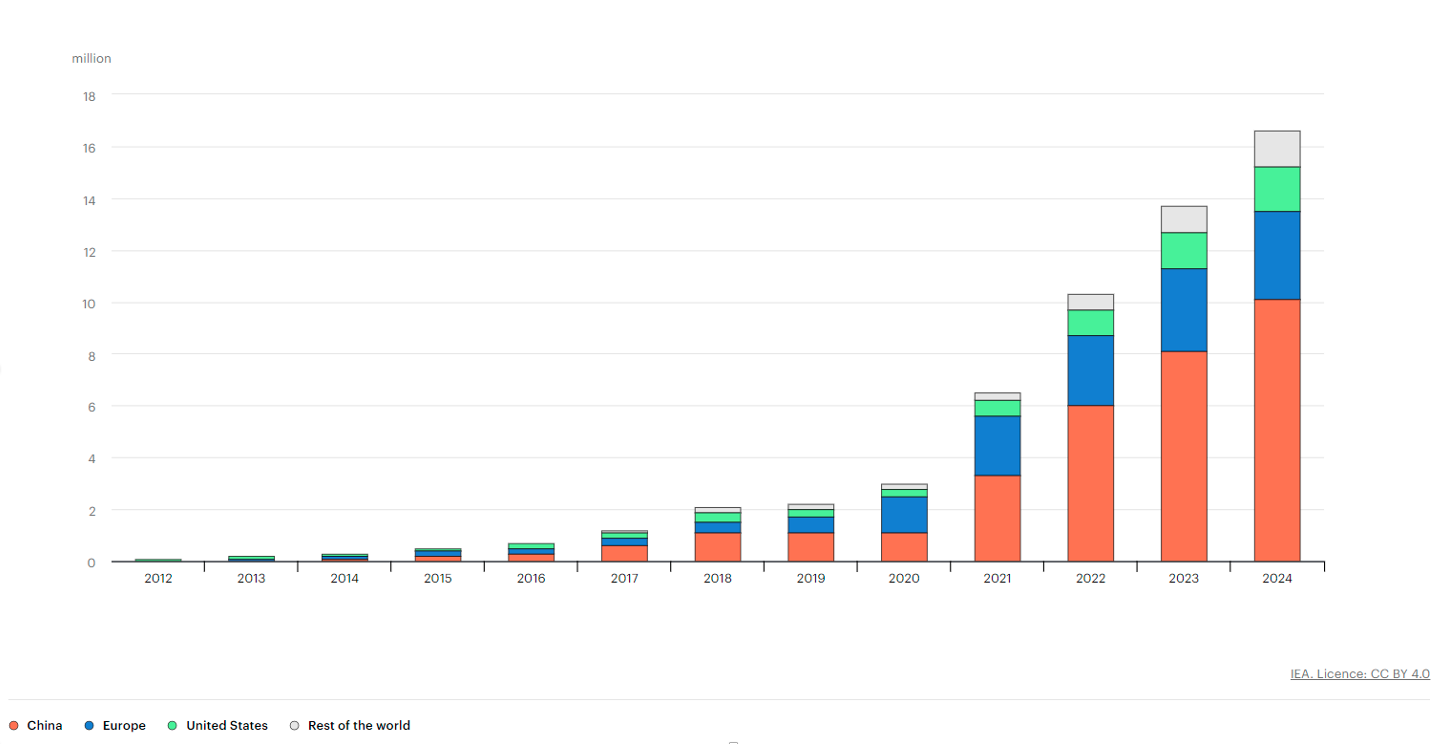

Electric vehicle (EV) demand has seen a meteoric rise for over a decade, transforming the automotive landscape. However, recent data reveals a surprising slowdown. For instance, while global EV sales reached 14 million in 2023, the growth rate has decelerated significantly compared to previous years. This article explores the reasons behind this slump, its impact on the industry and environment, and future outlooks.

Overview of the Slump in EV Demand

Historical Context

Over the last decade, the EV market has enjoyed robust growth, driven by technological advancements and substantial government incentives. Between 2018 and 2023, EV sales increased more than sixfold, even the Covid lockdowns did not dent the EV growth much. This growth trajectory now faces significant headwinds, leading to a reevaluation of future market dynamics.

Current Trends

Global EV sales increased by 35% in 2023, but this is a slowdown from the rapid growth rates of previous years. In 2022, sales grew by 65%, highlighting the current market's deceleration. The United States, Europe, and China remain the largest markets for now, yet each faces unique challenges.

The U.S. saw new registrations drop as high vehicle prices and limited charging infrastructure deter buyers. Similarly, Europe experienced a slowdown due to the phasing out of government subsidies in major markets like Germany and the UK.

Whereas China, despite experiencing a price war led by Tesla and BYD, is grappling with market saturation and economic slowdowns that have tempered its previously rapid growth trajectory. However, the Chinese market continues to dominate globally, driven by aggressive pricing strategies, a consolidated supply chain and healthy competition among domestic manufacturers

Factors Contributing to the Slump

Several factors contribute to the current slump in EV demand:

- • Economic Factors: Rising inflation and interest rates have made financing EVs more challenging for consumers. Combustion engines are still cheaper and more attractive, given the high financing rates.

- • Consumer Preferences: The cost of EVs remains significantly higher than that of traditional combustion engine vehicles. A report by Autoblog highlighted that prices for “affordable” EV models often range between $30,000 and $50,000, excluding additional costs such as insurance, taxes, and fees. This high initial cost is a major obstacle to widespread adoption, as many potential buyers are priced out of the market.

- • Market Corrections: According to IDTechEx, the current downturn is seen as a natural market correction following years of rapid growth. This adjustment is expected to stabilize the market, with long-term prospects remaining positive due to increasing regulatory pressures and technological advancements.

- • Economic Slowdown and Policy Changes: Insights from Goldman Sachs indicate that economic slowdowns and shifting policies are also crucial factors. Economic uncertainty reduces consumer spending power, while changes in EV-related policies in Europe and incentives can dramatically influence market dynamics. These aspects contribute to the decreased pace of EV adoption.

- • Automaker Adjustments: According to Nasdaq, traditional automakers have overestimated current demand levels and are adjusting by scaling back production and lowering prices. These adjustments come as automakers experience losses per EV sold, leading to a more cautious approach to future EV commitments.

Impact on the EV Industry

Major EV Manufacturers

The slump has significantly affected major EV manufacturers. Tesla reported a 14% decline in production in Q2 followed by a 9% drop in revenue in Q1 of 2024, leading to revised growth projections and a pushback in the date of its robo-taxi reveal. Volkswagen and BYD also scaled back production plans.

EV Supply Chain

The slowdown impacts the entire EV supply chain. Battery production has slowed because of reduced demand, resulting in a surplus of raw materials like lithium, cobalt, nickel, and copper. This surplus means that battery demand till 2030 is not likely to outpace supply and this is likely to depress prices, affecting mining companies and material suppliers in the short term.

Innovation and Research

With reduced revenue, many companies may cut back on innovation and research. This could delay advancements in battery technology and EV infrastructure, potentially stalling the sector's progress toward more efficient and affordable EVs but at the same time, this may make room for hybrid vehicles.

Environmental Considerations

The decline in EV demand poses significant risks to global climate targets. EVs are crucial for reducing carbon emissions in the transportation sector, which accounts for over 15% of global energy-related emissions. A prolonged slump could severely hinder the transition from fossil fuels to renewable energy sources. The decreased adoption of EVs could delay the widespread reduction of greenhouse gas emissions, affecting not just transportation but also the broader energy ecosystem and global climate initiatives. This is why the current slump in demand cannot become a prolonged trend. So let`s look at the likely scenarios that may change the trend.

Future Outlook

Potential Recovery Scenarios

Several recovery scenarios are possible:

• Government Incentives: Renewed or enhanced subsidies could boost EV sales making them more affordable as compared to combustion engines.

• Technological Advances: Improvements in battery technology and charging infrastructure can trigger another growth phase. Especially if the battery range can be increased significantly beyond what it is presently.

• Economic Stability: Stabilization of the global economy and lower financing rates could make EV financing more accessible.

Long-term Implications

In the long term, the EV market is likely to see consolidation, with stronger players surviving and smaller companies potentially exiting. This could lead to more sustainable growth rates and a resilient industry structure. The automotive industry might also see a shift towards hybrid models as an interim solution.

Asia and China in particular are going to be the next goldmine for the EV market. Whereas Europe and America are likely to see slow growth due to a multitude of factors, with protectionism against Chinese EV imports being the main factor.

Investor Takeaway

Despite the current challenges, strategic investors can find opportunities. It is important to remember that the EV market is still young and therefore likely to go through corrective phases. Mining companies supplying materials for EV production are likely to remain resilient, as the demand for these materials extends beyond just the EV industry. Investors should monitor recovery signals and market shifts to capitalise on new opportunities in the evolving EV landscape.

The future of EV demand is likely to see a very sustained level of growth. Investors who adapt and innovate may find themselves well-positioned to benefit from the next phase of this dynamic market.