The importance of copper in 2026

The importance of copper in 2026

Copper is at the centre of the most consequential economic shifts of our time. The red metal powers electric vehicles, solar panels, wind turbines, data centres, and military systems alike.

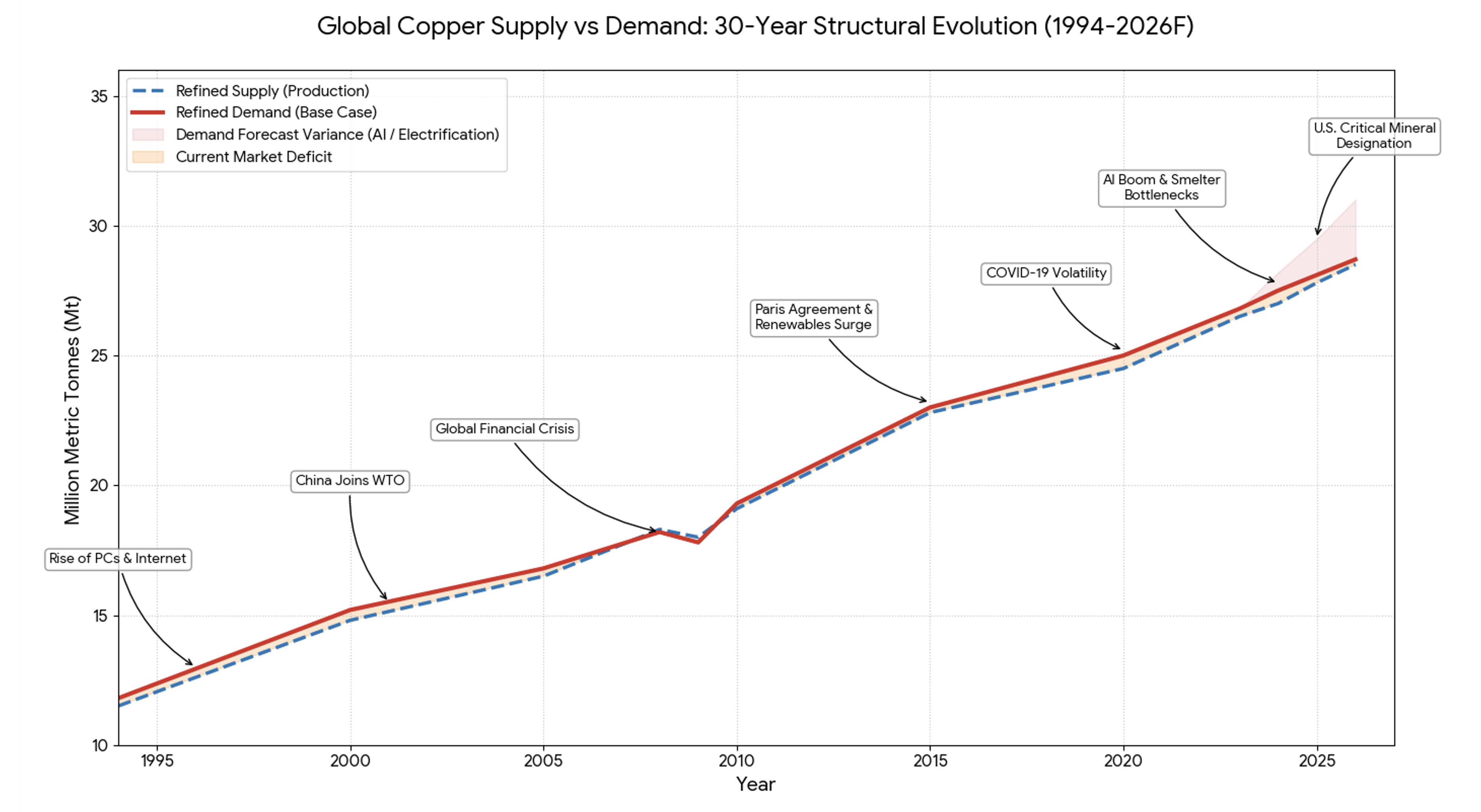

As of March 2026, this structural importance has manifested in a physical reality: the global copper market has transitioned into a structural deficit. With total refined demand projected to reach 28.7 million metric tonnes (Mt) against a tightening supply of just 28.5 Mt, the market faces an immediate shortfall of approximately 150,000 to 330,000 tonnes this year alone.

This mismatch between surging demand and constrained supply has elevated copper from an industrial staple to a high-stakes strategic asset. This is not a cyclical story, the forces reshaping the copper market are generational in nature and will outlast any single year's price action. We are no longer simply looking at a commodity cycle, but a permanent realignment of global infrastructure.

The Energy Transition: Copper's Most Powerful Demand Driver

The following 30-year data highlights a clear shift in the copper market's fundamental balance. From 1994 through the early 2020s, refined supply and demand largely moved in tandem, with periodic surpluses absorbing short-term shocks.

However, current 2026 data confirms a structural decoupling. As refined consumption reaches an estimated 28.7 million metric tonnes (Mt), it is outpacing refined production, which remains constrained at 28.5 Mt.

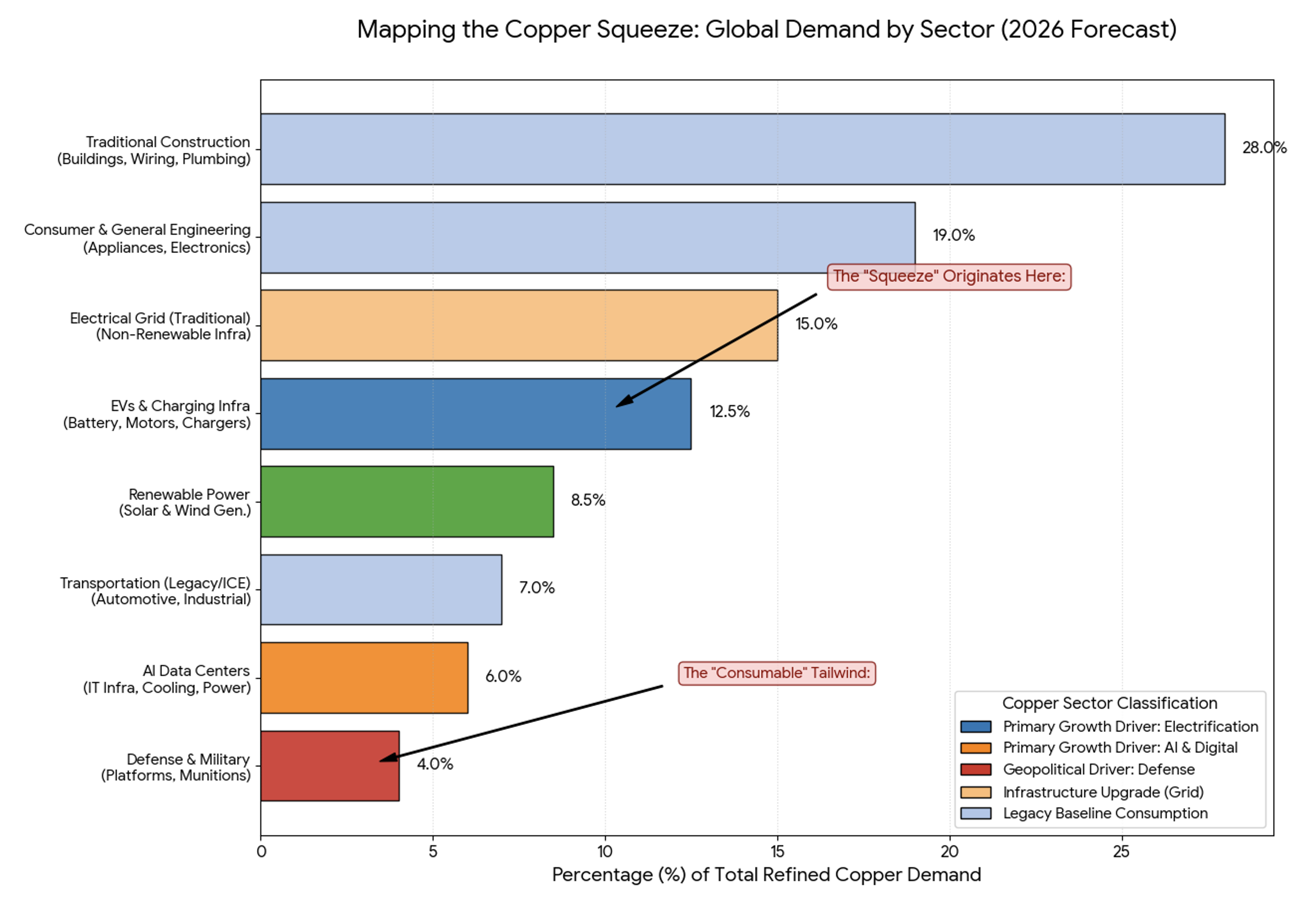

A single electric vehicle requires approximately 80 to 100 kilograms of copper, three to four times the amount found in a conventional internal combustion engine. A single megawatt of solar generating capacity requires around 5,000 kilograms for panels, cabling, and inverters. Wind turbines are similarly intensive. As governments across Europe, North America, and Asia race to meet decarbonisation targets, the cumulative copper requirements are staggering.

According to a January 2026 study by S&P Global, energy transition applications alone will account for 15.7 million metric tonnes of copper demand by 2040, the single largest growth segment in the global demand profile.

Global EV production is projected to exceed 30 million vehicles annually by 2026, meaning copper demand from vehicle manufacturing alone could approach 4 million tonnes per year, before accounting for the charging infrastructure and grid upgrades required to support them.

AI, Data Centres, and the Digital Infrastructure Boom

Artificial intelligence has rapidly emerged as one of the most consequential new demand drivers in the copper market. The physical infrastructure required to train and operate large language models and other AI systems is extraordinarily copper-intensive. Data centres consume copper at every layer: power distribution, server rack wiring, cooling systems, and the high-voltage transmission lines feeding their enormous appetite for electricity.

AI-optimised hyperscale facilities can require up to ten times the electrical load of a conventional data centre. A 2026 report by Morgan Stanley projects that global data centre copper consumption will reach approximately 740,000 tonnes in 2026, rising toward one million tonnes by 2027. By 2030, data centres could account for as much as 14% of total US electricity demand, with copper a critical enabler at every stage.

The scale of capital expenditure commitments from the world's largest technology companies ensures that this demand profile is structural, not cyclical. BloombergNEF analysis estimates that AI-driven demand growth could represent an incremental 2 million metric tonnes of copper consumption between 2025 and 2040 for IT infrastructure and associated power generation alone.

Defence Spending: An Overlooked Demand Catalyst

Global rearmament is a third structural tailwind for copper that is frequently underappreciated. Rising geopolitical tensions across Eastern Europe and the Indo-Pacific have prompted NATO members and allied nations to substantially increase defence budgets. Modern military platforms, from fighter aircraft and naval vessels to missile systems and surveillance infrastructure, are highly copper-intensive.

The S&P Global study projects global defence spending to double to approximately $6 trillion by 2040. This adds a layer of long-term copper demand that operates largely independently of the economic cycle, providing a degree of demand resilience that distinguishes copper from most other industrial commodities.

The Supply Deficit: A Structural, Long-Dated Problem

The demand case for copper would be compelling in any supply environment. Set against mounting supply constraints, the bull case becomes considerably more persuasive.

The copper market is transitioning from surplus to structural deficit. The International Copper Study Group (ICSG) has warned of a 150,000 tonne shortfall in 2026, having previously projected a surplus. J.P. Morgan's Global Research team forecasts an even sharper deficit of approximately 330,000 tonnes. Refined output is expected to grow by just 0.9% in 2026, down from 3.4% in 2025.

A series of significant supply disruptions compound this picture. The Grasberg mine in Indonesia, one of the world's largest copper producers, accounting for 3–4% of global output, was struck by a fatal mudslide and is not expected to resume full operations until well into 2027. Flooding has caused material delays at the Kamoa-Kakula complex in the Democratic Republic of Congo. In Chile and Peru, which together account for roughly 40% of the world's supply, declining ore grades and water scarcity continue to suppress output growth.

The longer-term supply picture is even more challenging. The average timeline from discovery to production has extended to 17 years globally and approximately 29 years in the United States due to regulatory complexity. Fewer than ten significant copper discoveries have been made globally in the past decade. BloombergNEF estimates the cumulative copper shortfall could reach 19 million tonnes over the next 25 years without new mines or significant gains in recycling capacity.

Price Outlook and Analyst Forecasts

Analyst forecasts for 2026 are broadly constructive, reflecting the structural supply-demand imbalance outlined above:

- J.P. Morgan projects a full-year average of $12,075 per tonne, with a Q2 peak near $12,500.

- Citigroup has outlined a bull case approaching $15,000 per tonne should supply shortfalls persist.

- Goldman Sachs projects a range of $10,000–$11,000, noting that strong demand from grid and power infrastructure is unlikely to permit a sustained decline below $10,000.

- The LME copper price touched a record $13,238 per tonne in January 2026, establishing a new high watermark for the commodity.

Macroeconomic tailwinds add further support. Anticipated Federal Reserve rate cuts in 2026 historically weaken the US dollar, making dollar-denominated commodities more affordable globally. China, which accounts for approximately 60% of global copper ore imports, has committed to "more proactive" fiscal and monetary policy, targeting grid upgrades, renewable energy projects, and data centre infrastructure. This provides a significant demand backstop.

The principal risks to the thesis centre on US trade policy and macroeconomic deceleration. Proposed tariffs of 10–15% on imported refined copper could distort global trade flows, while a sharper-than-expected slowdown in China could weigh on industrial demand. These risks are real but, in the assessment of most major institutional analysts, are insufficient to alter the fundamental direction of travel.

Investor Takeaway

The copper market in 2026 is driven by forces that are structural, well-capitalised, and accelerating. The red metal sits at the intersection of electrification, the clean energy transition, artificial intelligence infrastructure, and global rearmament. Each of these themes is durable and backed by committed capital spending running well into the next decade. On the supply side, a depleted project pipeline, extended permitting timelines, and acute mine disruptions combine to ensure the market cannot self-correct quickly in response to higher prices.

For investors with a multi-year time horizon, the case for copper is among the most compelling in the commodity complex.