The bank and my money

The bank and my money

Most people deposit money and then stop thinking about it. That gap between what you earn and what the bank earns is worth understanding, especially if you're sitting on significant capital.

When you deposit money at a bank, it doesn't sit in a vault with your name on it. The bank immediately puts that money to work by lending it out, buying government bonds, funding mortgages, and paying you a fraction of what it earns in return. This isn't a secret, but the mechanics are worth understanding if you're making serious decisions about where your capital lives.

The Spread is the Business

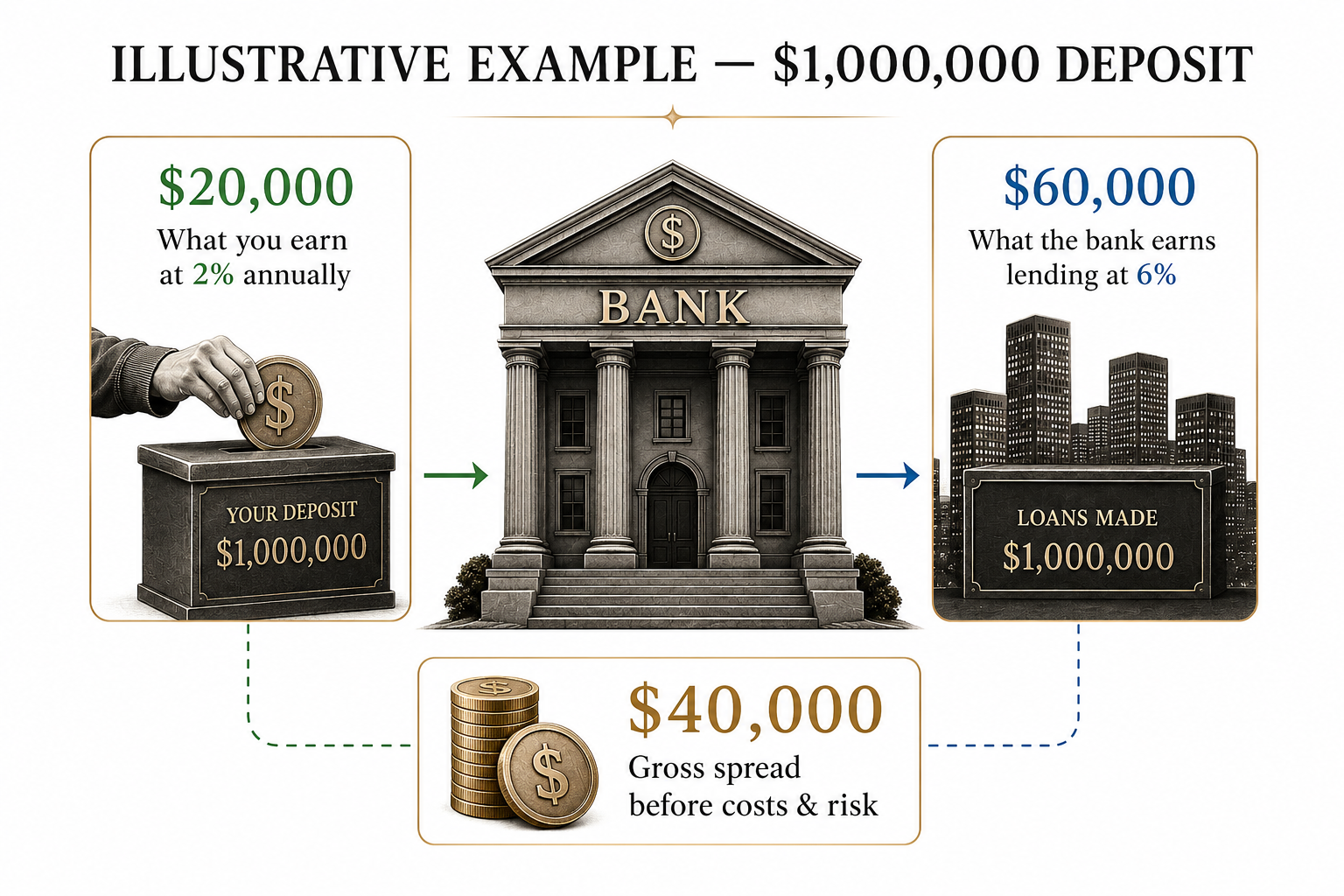

A bank's core profit engine is simple: borrow cheap, lend expensive. Your savings account might pay 1–4% annually. The bank lends that same capital at 6–25%, depending on whether it's a mortgage, a business loan, or a revolving credit facility. After accounting for staff, technology, defaults, and regulation, the difference is the net interest margin, and it's the primary reason banks are profitable.

That $40,000 isn't pure profit. The bank absorbs credit losses when borrowers default, carries the cost of regulatory capital requirements, funds deposit insurance schemes, and maintains the infrastructure that enables instant payments. Still, the economics reliably favour the institution over the depositor, and the gap tends to widen when central banks raise rates, since lending rates reprice faster than savings rates.

What the Bank Actually Does With Your Money

The largest use of deposits is lending: mortgages, business credit, consumer loans, and credit cards. These generate the highest yields and carry the highest credit risk. Banks also hold significant positions in government securities and central bank deposits, which offer lower returns but are liquid and essentially risk-free on a credit basis. Fees from payments, foreign exchange, wealth products, and merchant services add a third revenue layer that doesn't depend on interest rates at all.

"It's not your specific dollars being lent to someone else. Bank money is pooled. You hold a contractual claim on the institution — not ownership of any particular note."

What most people don't realize is that this dynamic applies to every account, not just savings products. A checking account earning nothing functions exactly the same way on the bank's balance sheet. Your money is still pooled, still deployed into loans and securities, still generating the same spread. The difference is that the bank's cost of funding drops to zero. They borrow your capital for free and lend it at 6–25%. In banking, these are called non-interest-bearing deposits, and they are among the most profitable funding sources a bank can have.

This became particularly visible after the rate hikes of 2022–2023, when banks earned 5% or more on deployed capital while millions of customers held checking accounts that paid nothing. The convenience of payment infrastructure, a debit card, and instant transfers is real, but it has a cost, and that cost is the yield you're not receiving. For anyone holding material cash in a non-interest account, the gap is worth quantifying.

The Risk That Regulation Exists to Contain

Maturity transformation creates a structural vulnerability: a bank run. If enough depositors lose confidence and withdraw at once, a solvent institution can become illiquid very quickly. Silicon Valley Bank's collapse in 2023 was a modern demonstration: a concentrated depositor base, rising interest rates eroding the value of long-duration bond holdings, and a withdrawal spiral that moved faster than regulators could contain.

The system's response to this vulnerability has several layers. Central banks act as lenders of last resort, providing emergency liquidity to solvent institutions facing short-term cash pressure. Deposit guarantee schemes: $250,000 per depositor per institution, administered by the FDIC in the United States, remove the incentive for small depositors to panic. Capital adequacy and liquidity coverage requirements force banks to hold buffers against stress scenarios. None of this makes the system failure-proof. It makes failure less likely and less catastrophic when it does occur.

Why Does This Matter if You Hold Significant Cash?

For most people, the mechanics above are academic. For those holding substantial sums in cash, whether as a liquidity buffer, pending deployment, or as part of a structural allocation, this is directly relevant. FDIC insurance covers up to $250,000 per depositor per institution, so large balances at a single bank carry unsecured exposure above that threshold. Net interest margin dynamics mean that the bank's rate-setting on savings products is an active choice, not a passive reflection of market rates. And the pooled, liability-based nature of deposits means that the credit quality of the institution itself matters in a way it doesn't for, say, a direct holding in a U.S. Treasury.

Investor Takeaway

Banks profit from your deposits, whether you're being paid for them or not. The spread exists regardless. The only question is how much of it you're leaving on the table. For transactional balances, that's an acceptable cost of convenience. For anything beyond that, it's worth a closer look.