Private equity explained

Private equity explained

Imagine two friends each invest $100,000. One buys public stocks such as index funds, blue chips, the usual. The other quietly puts money into a private equity fund. Twenty years later, their outcomes look radically different.

This is not a thought experiment. It broadly describes what happened to institutional investors who gained access to private equity in the 2000s versus those who did not. Private equity has long been known by name, misunderstood in practice, and accessible only to institutions and the ultra-wealthy. That is slowly changing, but before you decide whether it belongs in your portfolio, you need to understand exactly what you are getting into.

What private equity actually is

Private equity is capital invested in companies that are not publicly listed on a stock exchange. When you buy Apple shares, prices update by the second and you can sell tomorrow. Private equity does the opposite. It invests in private companies over long time horizons, with no daily price and no easy exit.

The term covers several distinct strategies:

Leveraged Buyouts (LBO): A private equity firm acquires a controlling stake in a mature company using a mix of fund equity and significant debt, often 40 to 70 percent of the purchase price. The firm improves the business and sells it at a profit, typically within five to seven years.

Venture Capital: Minority equity stakes in early-stage startups. Most investments fail or return modest multiples, but a single breakout like Sequoia backing Google in 1999 can return the entire fund many times over.

Growth Equity: Capital for established, profitable businesses that want to expand without giving up control. Lower risk than VC, lower return potential than buyouts.

Distressed: Buying debt or equity in financially troubled companies at steep discounts, then engineering a turnaround. High risk, potentially high reward.

How a PE Fund works

A private equity firm raises a fund from large investors such as pension funds, endowments, sovereign wealth funds, and wealthy individuals. These are called Limited Partners (LPs). The firm itself is the General Partner (GP).

The GP charges a management fee, typically 2 percent of committed capital annually plus carried interest. 20 percent of all profits above a hurdle rate, usually 8 percent per year. This is how private equity partners build significant personal wealth not from salaries, but from a share of the upside.

The fund lifecycle runs roughly as follows. Fundraising, then a 3 to 5-year investment period during which companies are acquired, then an active management phase focused on value creation, then exits via IPO, strategic sale, or secondary buyout, with proceeds returned to LPs. The full cycle typically takes 8 to 10 years.

In a fund's early years, returns look negative. Fees are being charged, capital is deployed into companies that haven't grown yet, and no exits have occurred. Only later, as portfolio companies are sold at a profit, does the return curve bend sharply upward. Impatience is one of the most expensive mistakes an LP can make.

The return premium — real or myth?

Private equity has long claimed to outperform public markets. The honest answer is that it depends a lot on the fund manager.

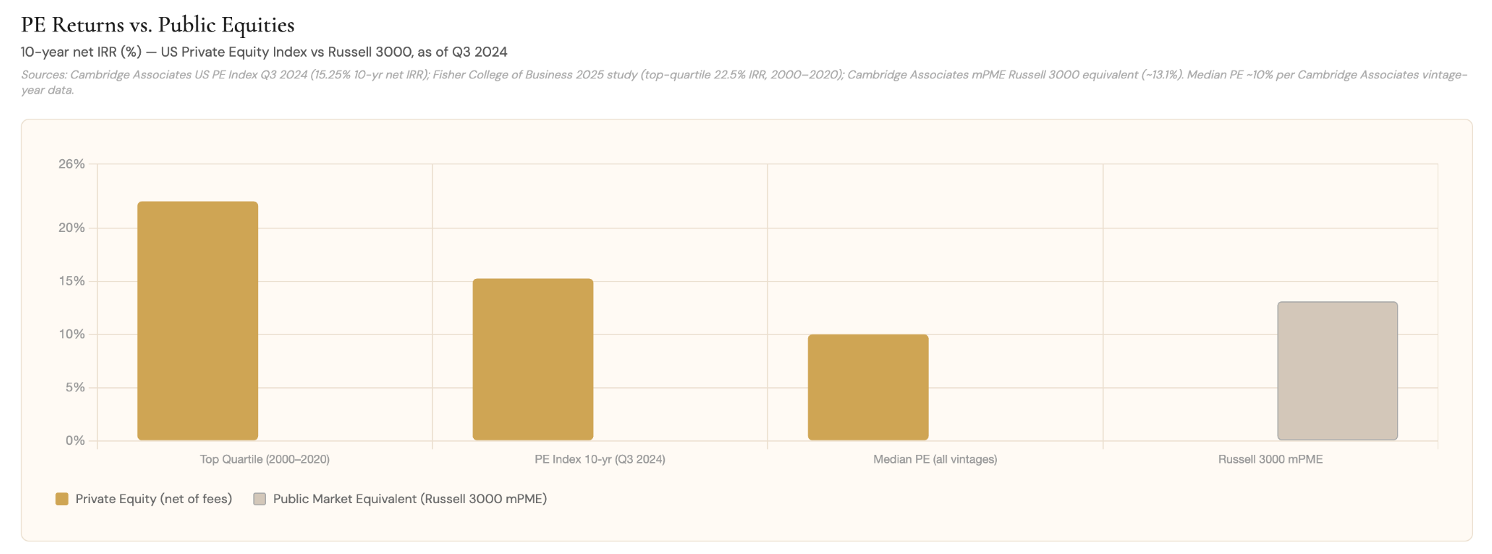

Top-quartile private equity funds have historically generated net IRRs around 22.5 percent over long periods, according to a 2025 Fisher College of Business study covering 2000 to 2020 vintages.

The broader US Private Equity Index, covering all 1,635 buyout and growth equity funds tracked by Cambridge Associates, returned 15.25 percent net over the 10-year horizon to Q3 2024, outpacing the Russell 3000 public market equivalent of 13.1 percent over the same period.

The median fund, however, clusters closer to 10 percent after fees, a modest premium over public markets that narrows further once you account for illiquidity and leverage. At the bottom quartile, private equity destroys value relative to simply owning index funds.

The critical variable is manager selection. The gap between top and bottom-quartile private equity managers is wider than in almost any other asset class. Unlike public equity markets, where most active managers cluster near the benchmark, in private equity the difference between a great fund and a poor one can be 15 percentage points of annualised return.

The question is never whether private equity can outperform. It can. The question is whether your private equity can.

How PE firms create value

Private equity firms typically pull three levers to generate returns.

Financial engineering: When KKR acquired RJR Nabisco in 1989 for $31 billion, the largest leveraged buyout in history at the time, roughly 90 percent of the purchase price was financed with debt. The logic is straightforward: if a firm puts in $300 million of equity to buy a $1 billion business and the company's own cash flows repay the debt over five years, the equity holders' returns are dramatically amplified relative to their initial outlay. The risk runs both ways — if the business deteriorates, the debt load accelerates losses just as quickly.

Operational improvement: When Hilton Hotels was taken private by Blackstone in 2007 for $26 billion, the firm spent the following years overhauling the brand's operations, expanding its loyalty programme, and growing its global footprint, free from the quarterly earnings pressure that shapes every decision a public company makes. By the time Hilton relisted in 2013, Blackstone had roughly tripled its equity investment. Private ownership creates the runway to make unpopular short-term decisions such as restructurings, leadership changes, and strategic pivots that public market investors would punish in the next earnings call.

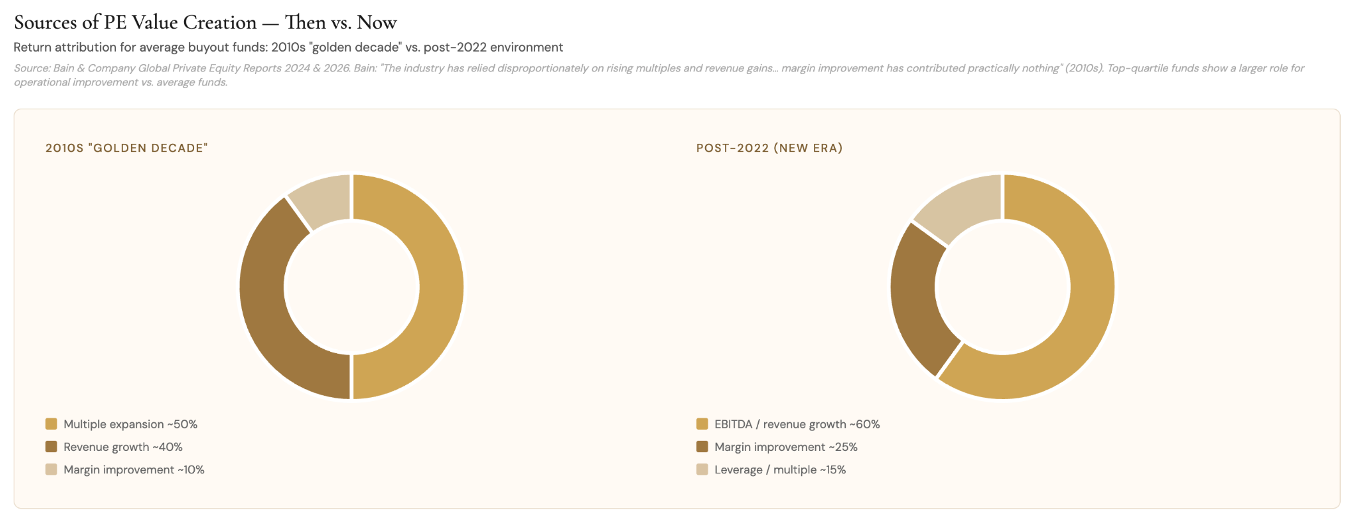

Multiple expansion: In the low-rate environment of the 2010s, private equity firms routinely bought businesses at 8 to 10 times EBITDA and sold them five years later at 12 to 14 times, not because the businesses had transformed, but because credit was cheap, buyer competition was fierce, and valuations drifted upward across the board. Bain's 2024 Global PE Report confirms that multiple expansion was the single largest driver of buyout returns across that decade. That tailwind has now largely reversed, which is why Bain argues that genuine operational improvement — not financial engineering or valuation arbitrage — is now the only reliable path to target returns.

Most successful buyouts combine all three. The best private equity firms are honest about which lever did the most work.

Key risks

Private equity's potential returns come with structural risks that are fundamentally different from those in public market investing.

- Illiquidity: Capital is locked for 7 to 10 years. No secondary market exit at fair value. Life events such as job loss and/or medical emergencies cannot be funded by this capital.

- Manager dispersion: As noted above, picking the wrong fund is extremely costly. Access to top-tier managers is the core challenge for non-institutional investors.

- Leverage risk: Rising interest rates, as seen in 2022 and 2023, increase debt service burdens on portfolio companies and can impair equity value significantly.

- Valuation opacity: Private equity holdings are marked-to-model rather than marked-to-market. Reported values are estimates, not verified prices, and can lag reality in both directions.

- Capital call risk: LPs must fund capital calls within days of notice. Failing to do so can result in penalties or forced sale of your LP interest at a loss.

How to access Private Equity

Traditionally, the minimum to invest in a flagship private equity fund was $5 to $25 million. That is changing, but the access point matters.

Listed PE firms: Blackstone (BX), Apollo (APO), KKR, Ares are publicly traded on stock exchanges. Buying their shares gives exposure to their fee income and balance sheet investments, with full daily liquidity. You are buying the management business, not a direct interest in portfolio companies, but it remains the most accessible and transparent entry point for most investors.

Evergreen and semi-liquid funds: Products like Blackstone's BREIT offer lower minimums ($25,000 to $100,000) and quarterly redemption windows. More accessible, but with different return characteristics than institutional flagship funds.

Fund of funds: A manager allocates across multiple private equity funds, providing diversification. The trade-off is a second layer of fees on top of the underlying fund's costs.

Is Private Equity right for you?

Private equity makes most sense when you have a genuine 10 to 12-year horizon with no anticipated need for the capital, a well-diversified liquid portfolio already in place, access to credible managers, and a clear-eyed view of the fee drag. For investors who meet these criteria, a 10 to 20 percent allocation to private markets has been supported by long-run evidence.

For everyone else, the listed private equity firms offer a reasonable way to participate in the sector's growth without a decade-long commitment. It is a different exposure but a real one.

The bottom line

Private equity is not magic. It is leverage, operational control, long time horizons, and illiquidity tolerance, applied to private companies with the goal of generating returns public markets cannot easily replicate. The best funds have done this extraordinarily well. Many have not.

Understand the mechanics. Scrutinise the fees. Be honest about your liquidity needs. And if you cannot access top-tier managers directly, the listed vehicles are worth understanding before assuming private equity is either off-limits or a guaranteed outperformer.

Private markets are no longer a secret. They are simply a discipline, one that rewards those who understand it.