Is my money safe at the bank?

Is My Money Safe at the Bank?

With the current recession affecting the financial markets and uncertainty hanging over people's savings, it's natural to look for ways to protect your money. Many may be wondering if their money is safe in the bank, or if they should be investing in stocks and other assets. In this article, we discuss the safety of leaving your money in the bank during a recession and explore why investing may be a better option for long-term security.

World bank cuts growth prospects

In its Global Economic Prospects report, the World Bank has reported a significant downgrade of global growth projections for 2023 compared to projections made in mid-2022. The organization forecasts that the total global economic growth will be 1.7%, far lower than its earlier prediction of 3%. This is due to what it sees as broadly worsening economic conditions across advanced economies.

The World Bank has also significantly reduced its growth outlook for China, Japan, Europe and Central Asia in 2023. In particular, its forecast for China declined to 4.3% from 5.2%, Japan slipped to 1% from 1.3%, and Europe and Central Asia were revised down to 0.1% from 1.5%.

With global economic activity slowing or even shrinking in some cases, keeping money stored in a bank may be considered as an effective way to protect it from inflation. However, this is only true if the interest rates are higher than the rate of inflation.

Are bank accounts worth it?

First, let us look at the benefits of keeping savings in a bank. One of the main advantages is that deposits of up to $250,000 are typically insured by the Federal Deposit Insurance Corporation (FDIC) in the US. Other countries also have similar regulatory bodies guaranteeing deposits up to a certain limit.

Additionally, banks offer a variety of savings accounts with different features, such as normal savings, high-yield savings accounts or certificates of deposit, which can help you earn a higher interest rate on your savings while having the liquidity and flexibility to withdraw your funds.

However, there are also some downsides to keeping savings in a bank during a recession. One of the biggest concerns is that interest rates on savings accounts are usually low compared to other assets and have historically not kept pace with inflation. This means that the buying power of your money may decrease over time.

The national average yield for savings accounts, as reported by Bankrate's weekly survey of institutions on January 18th, is 0.23 % APY. This yield for savings accounts is very low compared to the 6.5% multi-decade high rate of inflation, which means that the interest earned on savings accounts is nowhere near high enough to keep up with inflation. This can make it difficult for savers to maintain the purchasing power of their money over time.

This means that even though your money in the banks may be insured up to a certain limit, it doesn't mean that it's growing.

Better investment alternatives

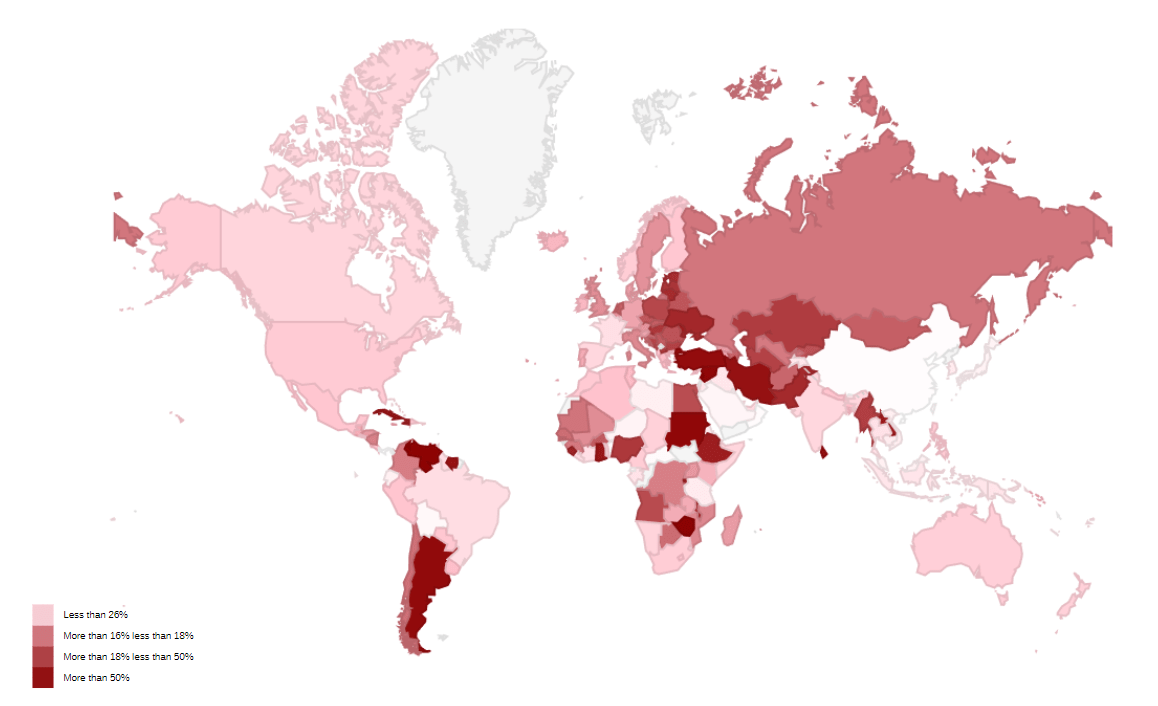

This map from December 2022 shows that, while North America and most of Western Europe have seen higher-than-usual inflation rates, these remain around or under the 15% mark. In contrast, inflation in developing countries concentrated in South Asia, the Middle East, Africa and South America is significantly higher, resulting in economic hardship along with unemployment, social unrest and political turmoil.

With the economic outlook uncertain and inflation on the rise in many countries, it's important to consider whether keeping your money in a bank is really worth it. This means that savers could see their purchasing power decrease over time. It's important for people to weigh these factors when deciding where to put their money during a recession.

So, what are some alternative options for saving money during a recession? One option is to invest in government bonds or Treasury bills, which are considered to be relatively safe investments. They are issued by the government and typically pay a fixed interest rate. Another option is to invest in stocks or mutual funds, which have the potential to provide higher returns over the long term but also come with a higher level of risk.

Another way to diversify your savings is investing in real estate, which can provide a steady stream of rental income and long-term appreciation, but it also requires significant capital and it may not be as liquid as other investments.

Investing in equity and commodities such as gold may be a better option for long-term security, given their ability to keep up with or even outperform inflation. This is because investments in stocks, commodities and other assets have better returns as compared to banks, helping to offset the impact of inflation.

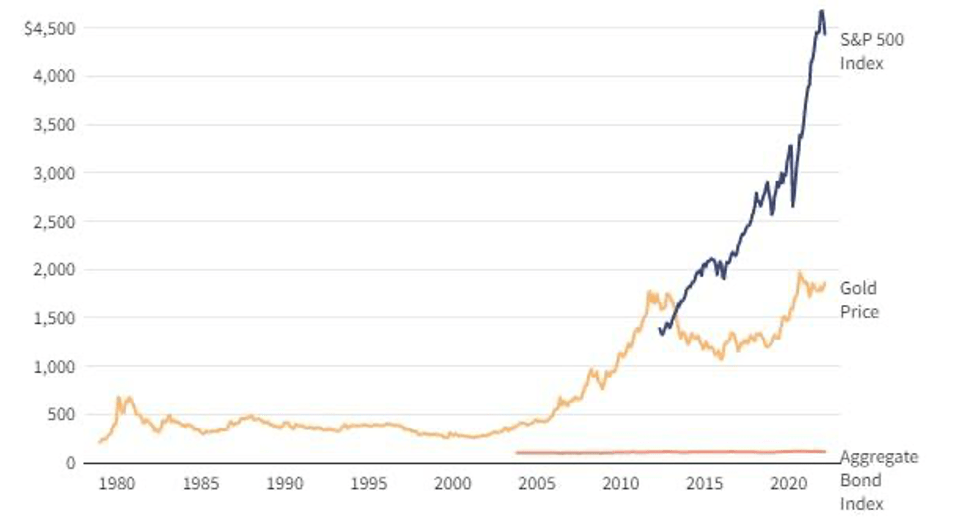

10 year Return on S&P500

Over the past 10 years, the S&P 500 has generated an average return of 14.83%, or 12.37% when adjusted for inflation - both significantly higher than the annual average return of 10%. Despite its fluctuations, only 2015 and 2018 resulted in losses, at 0.73% and 6.24% respectively.

15-year return on Gold

The performance of gold as an investment over the long term is dependent on the length of the time period analyzed. For instance, the above chart shows that in some 30-year periods, stocks have produced better returns than gold and bonds, while in 15-year periods, gold has surpassed stocks and bonds.

Overall, investing in equities and commodities such as gold are a better way to grow your money over the long term. These investments may be riskier than keeping your money in a bank account, but they also have the potential for greater returns. However, it's important to note that investing does come with risks. The stock market can be volatile, and the value of your investments can go up and down. But, over the long term, the stock market has historically provided higher returns than keeping your money in a savings account.

Another advantage of investing is that it can provide you with tax benefits. Certain types of investments, such as 401(k)s and ISA, offer tax-deferred or tax-free growth. This means that you don't have to pay taxes on the money that you earn from your investments until you withdraw it. This can help to increase the value of your investments over time.

Investor Takeaway:

In conclusion, saving money in the bank is a convenient option for many, but it may not provide the best protection from market volatility or inflation. Investing in assets such as stocks, mutual funds, real estate and commodities like gold can offer more security over the long term. It's important to take into consideration your own risk tolerance and financial goals when making decisions about your money. With the right strategy and knowledge, you can ensure that your money is safe and secure for years to come.