How inflation works

How Inflation Works

What 100 Years of History Reveal

Imagine placing $100,000 in a bank account in 2004 and leaving it untouched. Twenty years later, you open it, the balance intact, perhaps with modest interest. But here is the uncomfortable truth: in purchasing power, you may have lost a third of it. No theft. No bad investment. Just inflation, doing what it always does.

Most people think of inflation as a news story, a percentage flashed on television, a passing conversation about grocery prices. What they miss is that inflation is not an event. It is a force. Over a century of monetary history, it has reshaped fortunes and defined the difference between those who preserved wealth and those who watched it dissolve. Understanding it is essential.

What Inflation Actually Is

Strip away the jargon, and inflation has one meaning: your money buys less than it did before. Not because prices are misbehaving, but because the purchasing power of each dollar, euro, or pound has declined.

Think of it this way. A coffee that cost $1.20 in 2000 might cost $2.10 today. Your salary may have nominally risen, but if it hasn't kept pace, you are poorer in real terms. The same dynamic applies to housing, energy, education, and healthcare, the things that actually define living standards.

Economists measure this through the Consumer Price Index (CPI), a basket of common goods and services tracked over time. CPI is a useful proxy, but not a perfect truth. It may underweight housing costs in one era, or miss the specific inflation that hits retirees harder than young professionals. The number on the screen is a signal—not the whole story.

How Inflation Happens - Three Core Drivers

1. Demand-Pull Inflation

When too much money chases too few goods, prices rise. This is demand-pull inflation. The post-pandemic stimulus surge of 2020–2021 is a textbook example: governments injected trillions into economies while supply chains were frozen. Demand surged. Supply couldn't keep up. Prices followed.

2. Cost-Push Inflation

When the cost of producing goods rises, businesses pass those costs to consumers. The oil shocks of the 1970s are the defining case. Crude oil prices quadrupled almost overnight, rippling through every sector of the economy. Energy-intensive industries saw their margins collapse; consumers faced higher prices for everything from petrol to plastics.

3. Monetary Expansion

Central banks—the Federal Reserve and the European Central Bank—control the money supply. When they expand it faster than the economy grows, each unit of currency becomes worth slightly less. Over long periods, this is the dominant driver.

As economist Milton Friedman argued, inflation is always and everywhere a monetary phenomenon—a slow dilution of currency driven by the expansion of money supply over time.

What History Reveals in 100 Years of Inflation

Weimar Germany, 1921–1923: The Extreme Case

No historical example illustrates inflation's destructive potential more starkly than Weimar Germany. Following World War I, the German government printed money to pay war reparations. By 1923, hyperinflation had taken hold—prices were doubling not annually, but daily. Workers were paid twice a day so they could spend their wages before they became worthless. Lifetime savings were obliterated in weeks. A wheelbarrow of banknotes could not buy a loaf of bread.

The lesson: when trust in currency collapses, no nominal account balance offers protection. Currency risk is not theoretical, it is a historical fact.

The 1970s: Inflation Without End

The oil shocks of 1973 and 1979, combined with loose monetary policy, pushed inflation above 10% in much of the developed world. In the United States, inflation peaked at over 14% in 1980. Equity markets stagnated in real terms throughout the decade. Investors who held cash or long-duration bonds saw their wealth systematically eroded. The lesson: inflation can persist for years, not months, and it can coexist with economic stagnation, what economists call stagflation.

Post-2008: The Era of Hidden Asset Inflation

After the Global Financial Crisis, central banks deployed unprecedented monetary stimulus. The expectation was consumer price inflation. What happened instead was subtler: CPI remained low, but asset prices (stocks, real estate, private equity) surged. Wealth grew for those who owned assets; those who held cash watched their real purchasing power slowly erode. The lesson: inflation doesn't always show up where expected. It finds the path of least resistance.

Post-2020: The Return No One Was Ready For

The COVID-19 pandemic triggered the largest peacetime fiscal and monetary expansion in history. When supply chains fractured and demand surged simultaneously, inflation returned with force. By 2022, CPI in the eurozone had reached 10.6%, a level not seen in generations. The lesson: inflation can return rapidly after decades of dormancy. Complacency is expensive.

The Present: Geopolitics as an Inflation Engine

If the post-2020 surge was a warning, the years that followed confirmed something important: inflation increasingly wears a geopolitical face. Russia's invasion of Ukraine in 2022 removed one of Europe's largest suppliers of natural gas, wheat, and fertiliser from global markets almost overnight. Energy prices across the continent surged. Food inflation hit populations from Western Europe to North Africa. The war did not merely disrupt trade - it restructured it, forcing costly and rapid rewiring of supply chains that had taken decades to build.

Simultaneously, escalating tensions between the United States and Iran have kept pressure on the Strait of Hormuz, the narrow passage through which roughly 20% of the world's oil and a significant share of its liquefied natural gas flow daily. Any sustained disruption there would be transmitted instantly into global energy prices, echoing the supply-side dynamics of the 1970s oil shocks. Markets price in this risk continuously, and when tensions spike, so do commodity prices.

What these episodes illustrate is a broader structural shift: inflation in the modern era is no longer driven solely by monetary policy or domestic demand cycles. It is increasingly shaped by geographic chokepoints, energy dependencies, and the fragility of just-in-time global supply chains. The lesson is not that conflict always causes hyperinflation, but that the architecture of global trade now transmits geopolitical shocks into consumer prices faster, and with less warning, than at any prior point in history.

When Both Stocks and Bonds Fall Together

One of the most jarring financial lessons of recent years came in 2022, when equities and bonds fell sharply together. For decades, conventional wisdom held that a diversified portfolio, part stocks, part bonds, would cushion any single shock. But the inflation surge exposed a key limitation of that assumption. As pandemic-era price pressures intensified and the Federal Reserve raised rates at its fastest pace in decades, bonds sold off, while higher discount rates weighed on equities. The traditional hedge failed precisely when it was needed most.

Geopolitical escalation, including the Iran conflict and its pressure on commodity markets, has since kept the correlation between stocks and bonds elevated. High commodity prices percolate through corporate costs, compress margins, and weigh on equity valuations simultaneously with the bond losses that come from rising rates. The implication for investors is significant: in a sustained inflationary environment, the architecture of a standard portfolio may need to be rethought.

More recently, geopolitical escalation, including Iran-related tensions and their pressure on energy markets, has reinforced the same concern. Commodity shocks can feed inflation expectations, raise pressure on central banks to keep policy tight, and weigh on corporate margins. In that environment, equities can suffer from lower valuations and weaker margins while bonds suffer from rising yields. The implication for investors is significant: if inflation remains persistent, the standard stock-and-bond portfolio may provide less protection than it did in the low-inflation era.

Bull markets come and go. High inflation does lasting damage.

What Inflation Does to Bank Deposits - The Silent Impact

This is the most underappreciated dimension of inflation, and the most relevant for savers and wealth holders.

The Math Is Unambiguous

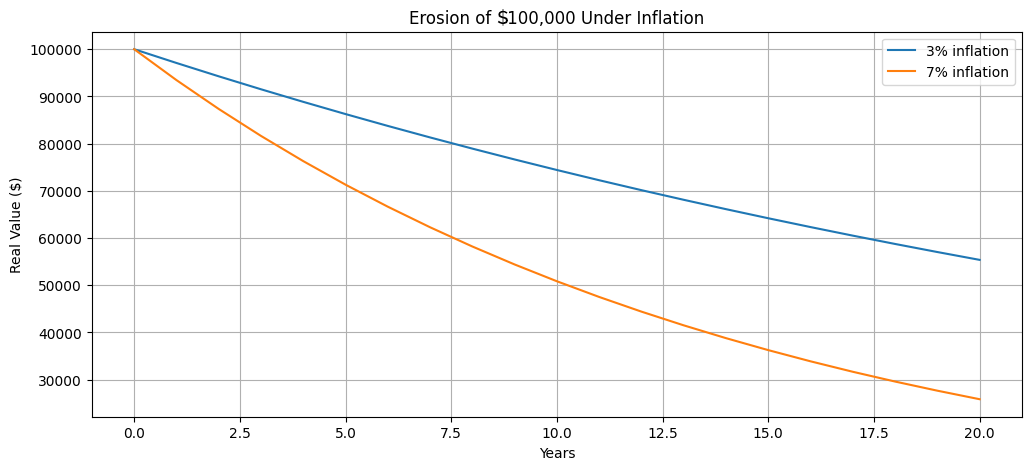

Consider $100,000 held in a bank account earning near-zero interest—a reality for many European depositors throughout the 2010s. At 3% annual inflation, that sum retains only about $55,000 in real purchasing power after 20 years. At 7% inflation, the same sum shrinks to roughly $25,000 in real terms. The nominal balance is unchanged. The real value is not.

The mechanism is compounding, working in reverse. Just as compound interest builds wealth, compound inflation erodes it. And it does so invisibly, without drama, without triggering an alarm.

The United Kingdom offers a recent and concrete illustration. In early 2023, British CPI remained in double digits for seven consecutive months, peaking above 10%. The practical consequence: £5 in 2023 bought only what £4 had bought in 2019. A 20% loss of purchasing power in four years, with cash balances nominally unchanged. European depositors faced a parallel reality, with eurozone inflation hitting 10.6% in 2022 while many bank accounts continued to earn near zero.

Even "safe" savings carry risk — the guaranteed risk of slow erosion when interest rates fall short of inflation. This is not speculation. It is arithmetic.

Why Inflation Hits Different People Differently

Inflation is not neutral. It redistributes wealth rather than simply reducing it.

- Wage earners lose if salary growth lags behind price increases, and their real income falls.

- Debtors benefit: a fixed mortgage or loan becomes cheaper in real terms as inflation rises. The debt doesn't change; the currency it's denominated in does.

- Savers lose: cash and low-yield deposits are the most vulnerable assets in an inflationary environment.

- Asset holders tend to fare better: real estate, equities, and commodities often retain or grow their real value over time.

This is why inflation is as much a political and social issue as an economic one. It quietly transfers purchasing power from those who hold cash to those who hold assets—widening the gap between savers and investors.

Thinking About Protection

Inflation protection begins with awareness, not products. The starting point is understanding that holding excessive cash over long time horizons is itself a decision, one with a measurable cost.

Basic Principles

- Avoid concentrating long-term wealth in low-yield cash or deposits.

- Diversify across asset types with different inflation sensitivities.

- Account for real returns, not just nominal ones, when evaluating any asset.

For More Advanced Consideration

Real assets like property, infrastructure, and commodities have historically provided inflation linkage. Equities in companies with pricing power (those able to raise prices in line with costs) offer a natural hedge over the long term. The logic is straightforward: equities tend to benefit from lower interest rates, and over time their growth has consistently exceeded inflation in most developed markets. This does not make them risk-free, as 2022 demonstrated, short-term drawdowns can be severe, but for long-term holders, equities have been among the more reliable tools for preserving real wealth.

Inflation-linked instruments, such as index-linked bonds, provide explicit CPI protection and should be included in a diversified portfolio. For retirement planning in particular, holding exclusively bonds carries a hidden danger: fixed income loses purchasing power in inflationary environments, and nominal stability is not the same as real security.

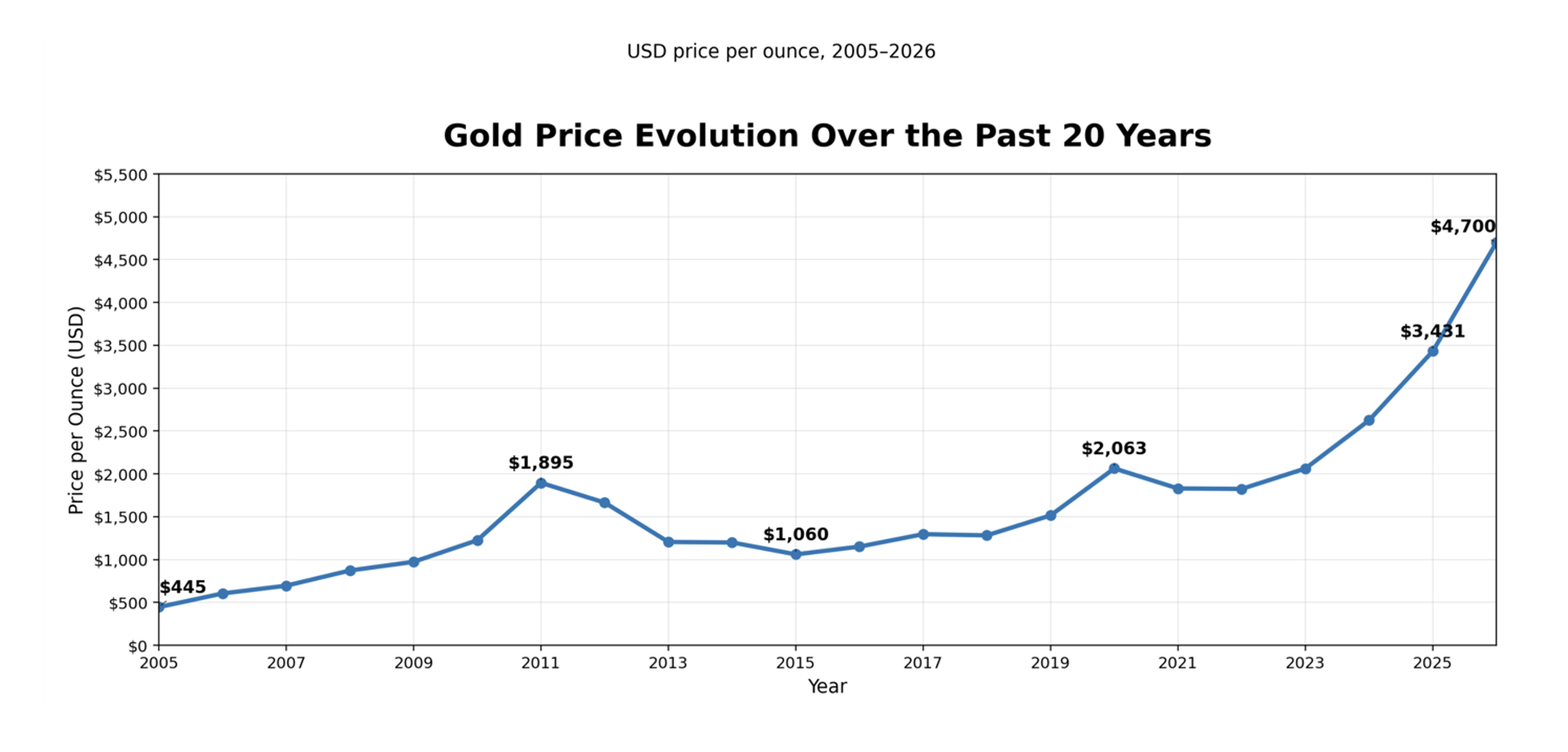

Gold occupies a distinct position in this discussion. Over the very long term, since 1900, the real price of gold has multiplied more than five times in US dollar terms, and over twelve times in sterling. Its track record as a store of value across centuries is genuine. However, that headline figure masks considerable volatility: a speculative bubble in the 1970s inflated gold prices dramatically, and by 2000 those gains had been almost entirely unwound. Gold is a long-horizon asset, not a short-term hedge, and its role in a portfolio should be sized accordingly.

Key Takeaways

- Inflation is compounding and cumulative—its impact is always larger than it appears in the short term.

- History demonstrates that inflation can accelerate suddenly, after years or decades of calm.

- Cash is nominally stable but unstable in real terms—the two are not the same thing.

- Inflation redistributes wealth; it does not merely reduce it.

- Long-term wealth preservation depends on one thing above all: consistently outpacing inflation in real terms over time.

The history of money is, in many ways, the history of inflation. Understanding it is the first step toward not repeating its most costly mistakes.