How gold protects portfolios

How gold protects portfolios

Why every portfolio needs gold and how much is enough

Gold's role in a portfolio is frequently misunderstood. It is not primarily a return-generating asset, though its long-term real return is positive and significant. Its primary function is correlation: gold tends to perform well precisely when other major asset classes perform poorly.

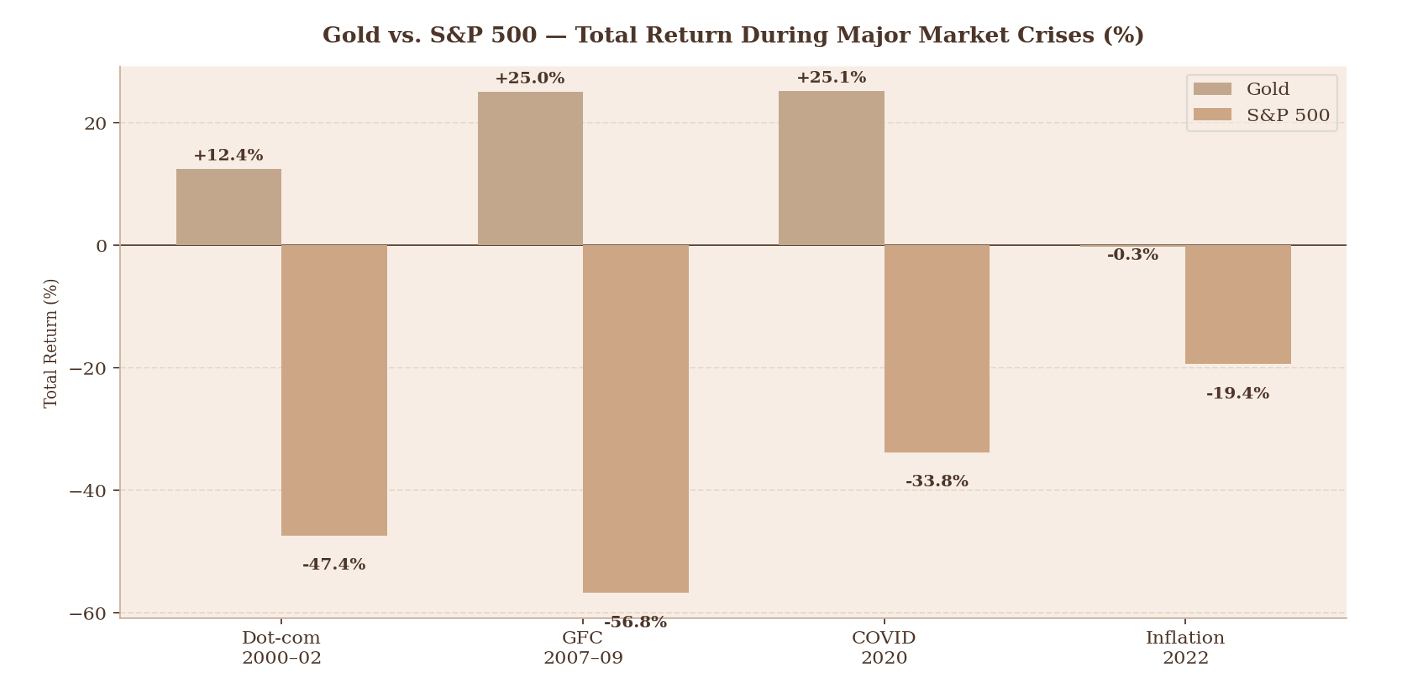

The data across multiple market crises is consistent. During the dot-com collapse of 2000–2002, the S&P 500 lost 47.4% of its value. Gold rose 12.4%. During the Global Financial Crisis of 2007–2009, equities fell 56.8%. Gold advanced 25%. During the COVID-19 shock of early 2020, gold rose 25.1%, while equities fell 33.8%. The one notable exception is 2022, where gold declined modestly alongside equities, though it still significantly outperformed bonds and most other assets in that environment.

Gold vs. S&P 500 total returns during major market crises. Source: Bloomberg / World Gold Council

The simplified version of Ray Dalio's All Weather Portfolio, one of the best-known risk-balanced allocation frameworks, includes a 7.5% allocation to gold because of its role as a diversifier, particularly in inflationary or market-stress environments. World Gold Council research also suggests that modest gold exposure can improve risk-adjusted returns and help reduce portfolio volatility and drawdowns over time, with many allocation studies pointing to a range around 5–10% depending on the investor's objectives and portfolio structure.

Gold does not just preserve wealth. It preserves optionality, the ability to rebalance into other assets at precisely the moment they are cheapest.

How much gold should you own?

There is no universal answer, but there is a coherent framework. The right allocation depends on risk profile, time horizon, existing portfolio composition, and view on macroeconomic conditions. What follows is a practical guide across investor profiles.

Conservative investor (capital preservation focus)

A 5–7% allocation to gold, primarily in physical form or gold-backed ETFs, provides meaningful downside protection without significantly reducing long-term growth potential. At this level, gold acts as insurance: a small cost in good times that pays off substantially in adverse scenarios.

Moderate investor (balanced growth and protection)

A 10–12% allocation is consistent with most institutional frameworks in periods of elevated macro uncertainty. At current levels of geopolitical tension, persistent inflation risk, and dollar pressure, this range represents a well-supported base case. A mix of physical gold, ETFs, and selected gold equity exposure provides diversification within the allocation itself.

HNWI / sophisticated investor (real asset orientation)

Allocations of 15–20% are not uncommon among family offices and high-net-worth individuals with long time horizons and real-asset mandates. At this level, gold functions as a core holding rather than a hedge — one component of a broader strategy that may include silver, resource equities, and direct commodity exposure. Some of the most risk-aware institutional investors, including central banks, have moved significantly beyond these levels in recent years.

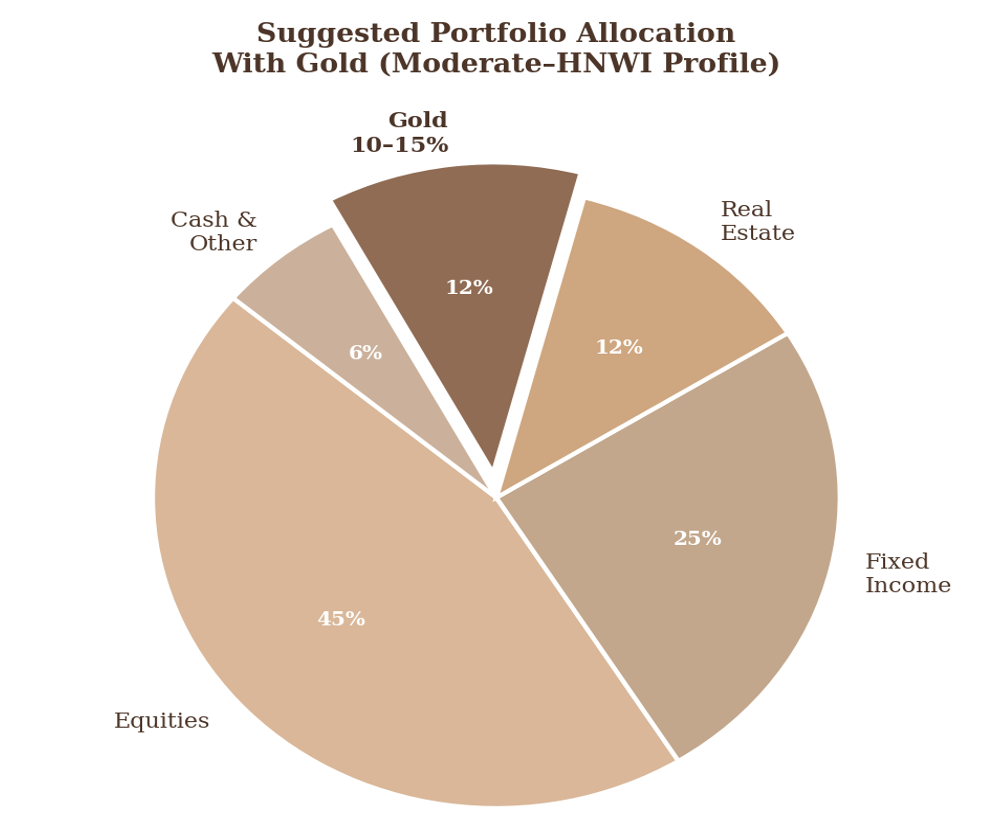

Illustrative portfolio allocation with gold for a moderate-to-HNWI investor profile

Investor takeaway

Regardless of investor profile, the case for holding some gold is difficult to ignore. A portfolio with no gold may still be diversified, but it lacks one of the few assets historically valued for its independence from currencies, governments, and the traditional stock-bond relationship. In an environment shaped by currency debasement, geopolitical shocks, and the failure of traditional diversification in periods such as 2022, gold deserves serious consideration as part of a broader wealth-preservation strategy.