Gold is a Tier I Asset – What Does This Mean?

Gold is a Tier I Asset – What Does This Mean?

Gold’s allure spans centuries, from ancient civilisations to modern financial markets, symbolising wealth, stability, and resilience. In the evolving global financial system, its prestige has been further reinforced under the Basel III framework, which recognises allocated gold as a high-quality, low-risk asset on par with cash and top-tier government bonds in terms of creditworthiness and liquidity.

This elevated status, solidified in the fallout of the 2008 financial crisis, highlights gold’s role as a strategic asset for institutions and investors alike, offering a trusted hedge against volatility and systemic risk. For investors seeking to position themselves for long-term security and upside potential, understanding gold’s enhanced regulatory treatment is key.

Decoding Tier I Assets

Tier I assets are the bedrock of a bank’s financial resilience, as defined by the Basel III accords, a global regulatory framework established by the Basel Committee on Banking Supervision (BCBS). These assets carry a 0% risk weight, meaning banks can hold them without reserving additional capital to cover potential losses.

Examples include cash, high-quality government bonds, and, crucially, physical gold held in allocated accounts (gold physically stored and specifically assigned to the owner). The World Gold Council emphasizes that “gold bullion held in own vaults or on an allocated basis is treated as cash and therefore risk-weighted at 0%”.

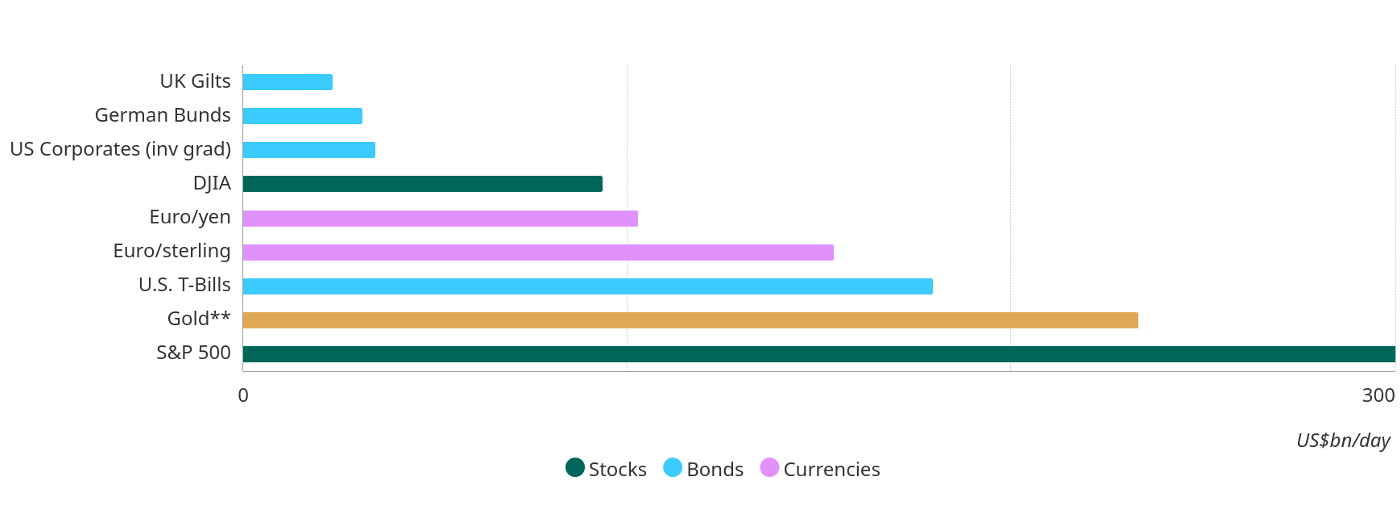

Average daily trading volumes for gold and other major asset classes in US$bn

Gold’s inclusion in this elite category is driven by its intrinsic qualities:

- Global Liquidity: Gold’s daily trading volume in 2024 averaged $233 billion, rivalling major forex markets.

- Zero Counterparty Risk: Unlike bonds or equities, gold’s value is independent of any issuer, making it immune to default.

- Safe-Haven Appeal: Historical data shows gold prices surged 78% from $730 to $1,300 between October 2008 and October 2010 during the financial crisis.

- Finite Supply: With annual mine production at approximately 3,661 tons in 2024, gold’s scarcity supports and in many ways increases its value.

Gold’s Regulatory Transformation Post-2008

The 2008 financial crisis exposed systemic vulnerabilities, with banks crippled by overexposure to risky assets like mortgage-backed securities. Under the Basel II framework, gold’s treatment was inconsistent, often classified with a 50% risk weight, requiring banks to hold substantial capital against it. This deterred banks from prioritising gold over cash or bonds.

The crisis, however, showcased gold’s resilience. While global equities fell 40% in 2008, gold prices rose, doubling from $700 in 2007 to $1,400 by 2011.

Recognising gold’s stability and role as a low-risk asset, BCBS revised its regulatory treatment under the Basel III framework. In 2017 guidance, the BCBS clarified that allocated gold bullion held in a bank’s own vault or through a low-risk custodian may receive a 0% risk weight for credit risk purposes, similar to the treatment of cash or sovereign bonds. This favourable classification enhances gold’s appeal for institutional investors and banks managing regulatory capital and liquidity requirements.

This reclassification was a game-changer. By aligning gold’s regulatory treatment with its market performance, Basel III positioned it as a stabilizing force for banks and the broader financial system.

Implications for Investors

Gold’s Tier I status reshapes its investment landscape, offering compelling opportunities:

- Rising Institutional Demand: Banks, incentivised to hold gold to meet Basel III requirements, are driving demand. Central banks purchased over 1,044 tons of gold in 2024, the third consecutive year above 1,000 tons, led by countries like China and India. This trend could push gold prices higher, with forecasts suggesting $3,000 per ounce by 2026.

- Regulatory Endorsement: Gold’s zero-risk status enhances its credibility. The reclassification has directly contributed to gold’s price appreciation due to increased bank holdings. This validation attracts institutional and retail investors alike.

- Shift to Physical Gold: Basel III’s focus on allocated gold may reduce speculative trading in paper gold, stabilising prices. Investors may favour physical gold or fully backed ETFs, aligning with regulatory preferences.

- Portfolio Diversification: Gold’s low correlation with equities makes it an ideal diversifier.

- Inflation Hedge: With global money supply having surged during the pandemic and remaining elevated in key economies, gold continues to serve as a hedge against currency debasement. The People’s Bank of China’s purchase of 225 metric tons of gold in 2023, its largest annual acquisition in decades, demonstrates a clear move by central banks to strengthen reserve portfolios against long-term monetary risks.

- Systemic Resilience: Gold’s role in bank balance sheets bolsters financial stability, indirectly supporting investor confidence across asset classes.

These dynamics make gold a strategic asset for investors seeking stability and growth in a volatile economic environment.

Strategic Portfolio Integration

To harness gold’s Tier I status, investors can adopt a disciplined approach.

- Core Allocation (5-15%): Experts like Ray Dalio advocate for a 5-15% gold allocation to optimise risk-adjusted returns. This balances stability with exposure to other assets. For example, a $1 million portfolio with 10% in gold ($100,000) would have mitigated losses during the 2008 crash, when gold gained 5% while equities fell 40%.

- Prioritise Allocated Gold: Focus on physical gold (bars, coins) or ETFs backed by allocated gold, such as SPDR Gold Shares (GLD), which holds physical bullion. Physical gold requires secure storage, but ETFs offer liquidity with expense ratios as low as 0.18% annually.

- Tactical Timing: Increase gold exposure during high inflation (e.g., 7% in 2022) or geopolitical tensions, as seen during the 2011 European debt crisis when gold hit $1,825. Monitor indicators like the Consumer Price Index or geopolitical risk indices.

- Diversified Exposure: Incorporate gold mining stocks for leverage to price increases, though they carry operational risks. Gold-focused mutual funds offer diversified exposure.

- Long-Term Commitment: Gold’s value has risen 650% since 1990, outpacing inflation and cash. Treat it as a store of value, not a speculative asset.

| Investment Option | Advantages | Risks | Ideal Investor |

|---|---|---|---|

| Physical Gold | Regulatory alignment, no counterparty risk | Storage costs, illiquidity | Long-term, risk-averse investors |

| Gold ETFs | High liquidity, low fees | No physical ownership | Convenience-focused investors |

| Gold Mining Stocks | High return potential | Company-specific risks | Risk-tolerant investors |

| Gold Funds | Broad exposure | Management fees | Diversification seekers |

Conclusion

Gold as a Tier I asset heralds a new era for this timeless asset. For investors, this status amplifies gold’s appeal as a safe-haven, diversification tool, and hedge against inflation and currency risks. With central banks purchasing over 1,000 tons annually and forecasts projecting $3,000 per ounce by 2026, gold presents a compelling opportunity.

Gold is not just an investment; it’s insurance against systemic failure. By strategically integrating gold into portfolios, investors can leverage its regulatory-backed stability to navigate an uncertain economic landscape.