Can copper supply meet demand in 2026?

Can copper supply meet demand in 2026?

Imagine a new AI supercomputing data center humming in the desert, miles of high-voltage lines linking offshore wind farms to cities, and EV charging corridors along every highway. These visions of the future have one critical element in common: copper.

Copper is quietly embedded in everything from power transformers and EV chargers to the vast wiring of data centers. Its unrivaled electrical conductivity and reliability make it nearly irreplaceable at scale. Aluminum, the nearest alternative, carries only ~60% of copper’s conductivity.

Lately, copper has shed its reputation as just another commodity and is increasingly viewed as a strategic “infrastructure metal” underpinning the green energy transition and the data economy. This shift raises a trillion-dollar question for 2026: Can copper supply keep up with surging demand, or are we heading into a major shortfall?

The 2026 setup: from small surplus to deficit

By late 2025, the market was already signaling tightness. LME inventories were sliding toward multi-year lows, a meaningful portion of remaining stock was already tied up for delivery, and 2026 treatment and refining charges (TC/RCs) fell to record lows.

On the demand side, large banks stayed constructive. Goldman Sachs, for example, projected copper to average about $11,400 per tonne in 2026, citing resilient electrification and grid demand against constrained mine supply.

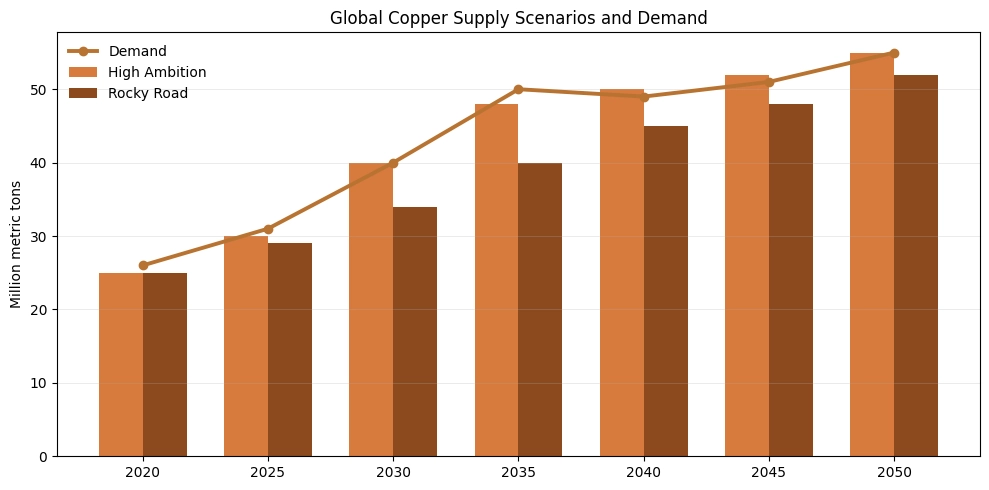

Industry forecasts suggest 2025 was the last year of a brief “breather.” The International Copper Study Group (ICSG) revised the 2025 surplus down to ~178,000 tons due to unforeseen mine setbacks, and many forecasts now point to a pivot into a deficit in 2026.

Source: S&P Global

Industry expectations put the 2026 deficit at ~150,000 tons, with inventories already relatively low and speculative positioning bullish, which means the market is on a knife-edge.

Copper doesn’t need a monster deficit to behave like a scarcity asset. When inventories are thin, and a chunk of stock is already reserved for delivery, small shortfalls can trigger sharp price moves.

Demand in 2026: the “three-engine” thesis.

Copper demand isn’t a one-trick pony (EVs) or a single headline (AI). It’s being pulled by three large engines at once.

1) Grid infrastructure: the green transition’s most copper-intensive layer

The push to modernize and expand electric grids is arguably the most copper-heavy part of electrification. Renewables, EV adoption, and industrial electrification all force upgrades to transmission and distribution lines, substations, transformers, and “last mile” upgrades. Copper is the preferred conductor because it conducts electricity efficiently with minimal losses.

Georgia Power projects it needs 10,000 MW of new capacity over the next five years, and says 80% of that is expected to serve new data centers. That implies miles of new transmission and substation work, loaded with copper.

This is the “boring but huge” driver for copper. Grids aren’t optional, and grid upgrades tend to be multi-year capex cycles.

2) AI & data centers: the copper story behind the screen

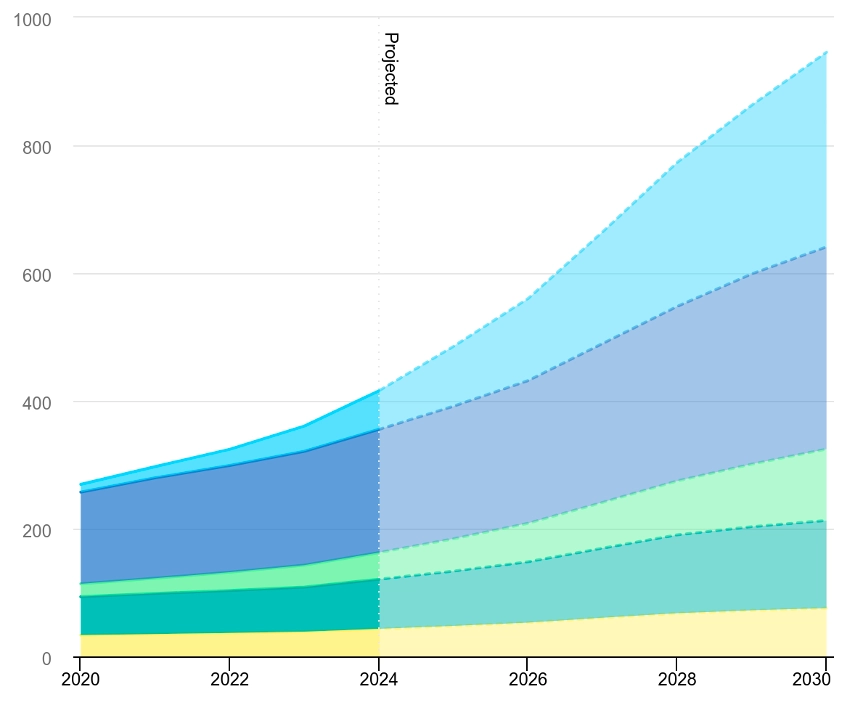

AI is digital, but its footprint is physical. Global data center electricity consumption was estimated at around 415 TWh in 2024 (~1.5% of global electricity use) and is projected to rise materially toward 2030.

Source: IEA

Why should investors care? Because data centers require copper in two places:

• Inside the facilities: miles of cabling, extensive cooling systems, transformers, switchgear. A Microsoft hyperscale data center used about 2,177 tonnes of copper, roughly 27 tonnes per MW of capacity, and AI-focused buildouts are even more copper-dense due to higher power and cooling intensity.

• Outside the facilities: The grid reinforcement to deliver reliable power. Utilities in multiple regions are racing to expand capacity and transmission to support these loads.

To put it simply, AI growth converts into copper demand via electricity and grid buildout.

3) “Baseline” demand: construction + industrial electrics still matter

Even if EVs and AI dominate headlines, copper’s demand base remains broad: construction wiring, appliances, industrial motors, and general electrical equipment. That base demand becomes the floor; electrification and AI become the incremental upside.

Supply side: why copper can stay tight even when “mine output is rising”

A useful way to think about copper is as a supply chain, not a commodity ticker. Availability depends on more than what mines dig out of the ground. It depends on whether there’s enough concentrate of the right quality, whether smelters and refiners can process it profitably, and whether inventories and logistics can bridge gaps.

China processes over 50% of the world’s refined copper, and in late 2025, there were reports that Chinese smelters agreed to cut output by over 10% in 2026 because processing fees were so low. Consistent with a concentrate shortage relative to smelting capacity.

ICSG projections show this choke point: refined copper production growth could slow to +0.9% in 2026, even if mine output grows by ~2.3% because concentrate availability is limited and scrap can’t fully close the gap.

Add in logistics, concentrate quality issues, and long supply chains, and you get the classic “headline supply rises, but the market still feels tight” setup.

When you put the moving parts together, the math isn’t complicated. If global copper demand grows around ~2% while refined copper production grows under 1%, you don’t need dramatic assumptions to land in a deficit. That sort of gap typically translates into a shortfall in the 100,000–150,000 ton range, roughly in line with the common ~150,000 ton deficit view.

Where it gets interesting for investors is what happens around that base case.

The bullish price scenario doesn’t require a whole new story; it just requires the existing one to run a little hotter. A demand upside surprise (stronger electrification spend, faster data-center rollout) or a supply hit (mine disruptions, tighter concentrate availability, smelter constraints) can widen the deficit quickly.

And that leads to the key market dynamic: asymmetry. When inventories are already low, and concentrate is tight, the market has less buffer. Upside shocks can push prices higher faster than downside shocks pull them lower, especially if the forward curve starts signaling scarcity through backwardation (near-term copper trading at a premium).

Risk factors

Copper may have structural tailwinds, but it’s still a cyclical asset, and tight markets can be interrupted. The main risk factors to watch are:

-

• Macro slowdown/recession: weaker construction and manufacturing demand can quickly soften the market.

-

• Project delays: grid upgrades and big capex cycles don’t move in a straight line; delays can push demand out by quarters.

-

• China demand surprises: China’s imports and domestic activity can swing the global balance meaningfully in either direction.

-

• Supply outperformance: mines ramping better than expected or fewer disruptions can relieve pressure faster than the market expects.

None of these invalidate the long-term electrification story. But they can change the 2026 price action, and price action is what investors are really trading.

Investor Takeaway

Copper is setting up like a tight-market trade into 2026. Inventories are low, TC/RCs have collapsed (a concentrate/refining constraint signal), and consensus is moving toward a 2026 deficit, which means the market has less cushion if anything goes wrong on supply.

If 2026 does land in a deficit, copper is likely to trade more like a strategic infrastructure asset than a slow-moving industrial commodity because electrification and AI are turning power buildout into a multi-year copper-demand cycle.

The bottom line is that the world is building more electricity infrastructure than the supply chain can comfortably support. This, in simple terms, is the case for the copper bull run for years to come.