Are gold and silver the best metals to own in 2026?

Are gold and silver the best metals to own in 2026?

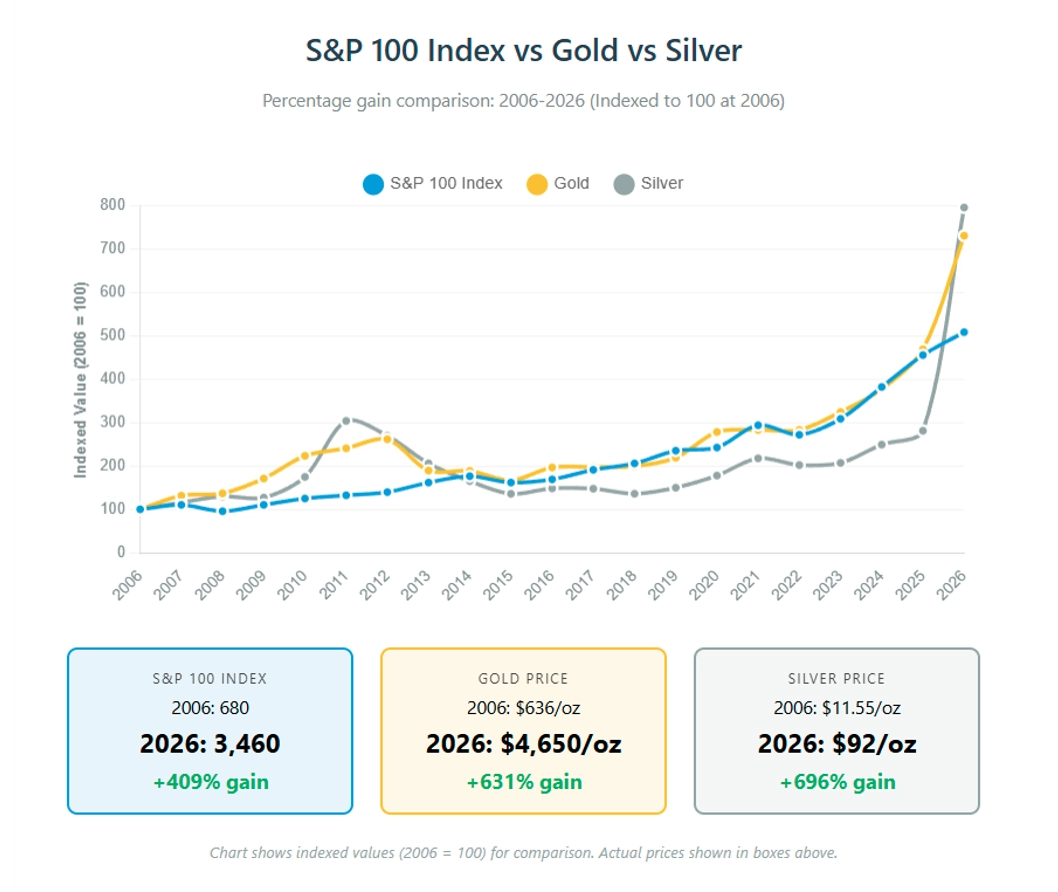

The answer for investors seeking crisis protection and portfolio resilience appears increasingly affirmative. Gold has shattered records, surging past $4,670 per ounce in January 2026, which is a stunning 67% gain over the past year and its strongest annual performance since 1979.

Silver has outpaced even gold, rocketing above $94 per ounce for the first time in history, delivering a remarkable 147% return in 2025 alone. These aren't speculative bubbles but reflect a fundamental shift: central banks are hoarding gold at record pace, industrial demand for silver is surging, and a volatile geopolitical landscape has reignited precious metals' ancient role as stores of value.

Central banks are buying gold at unprecedented rates

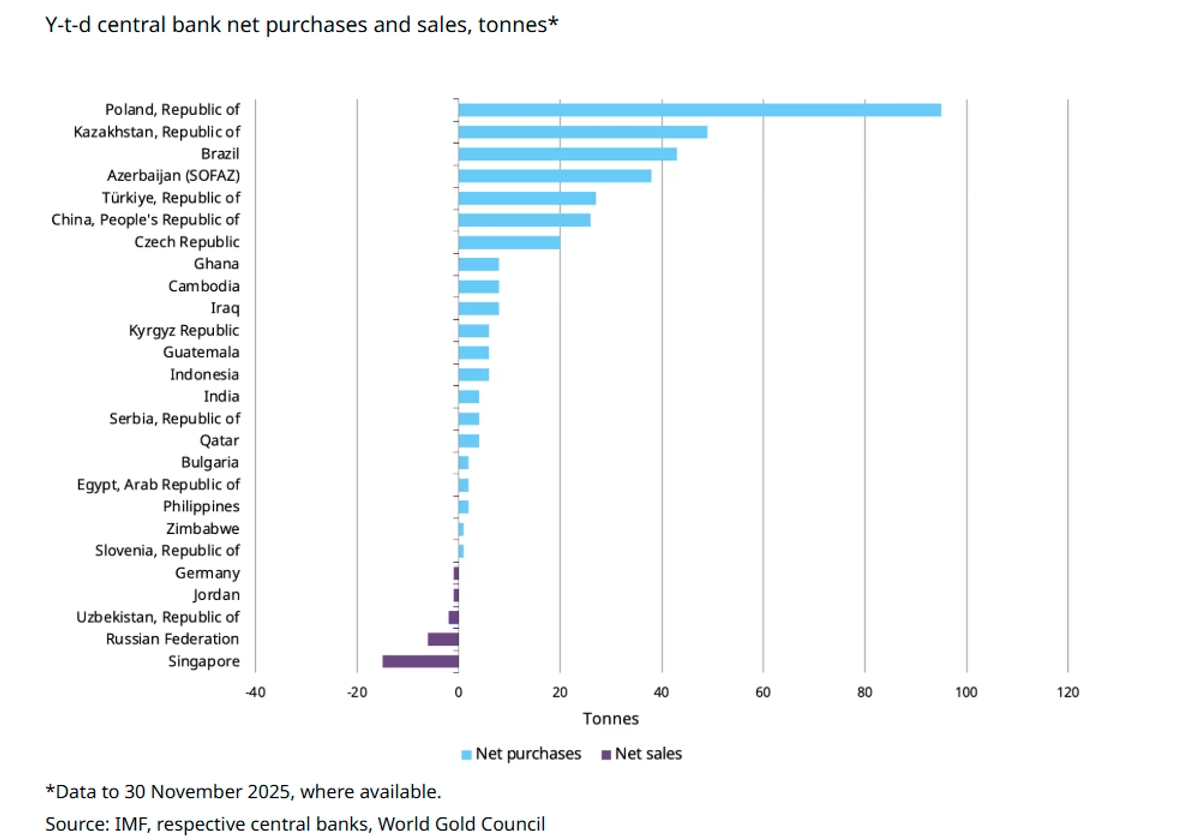

Perhaps the most powerful validation of gold's investment case comes from the world's monetary authorities themselves. Central banks purchased 1,045 tonnes of gold in 2024, the third consecutive year exceeding 1,000 tonnes and roughly double the annual average from the prior decade.

Poland led buyers with 90 tonnes, targeting 20% of reserves in gold. Turkey added almost 30 tonnes, and China officially accumulated almost the same amount.

The motivation is clear. After Western nations froze approximately $300 billion in Russian reserves following the 2022 Ukraine invasion, central bankers globally recognized a sobering reality: dollar-denominated assets can be weaponized.

Gold cannot be frozen, printed, or sanctioned. A 2025 World Gold Council survey revealed that 95% of central banks expect global gold reserves to increase, with 43% planning to add to their own holdings.

J.P. Morgan projects that central banks and investors will demand approximately 585 tonnes per quarter through 2026, providing structural price support regardless of short-term volatility.

Multiple geopolitical crises fuel safe-haven demand

Unlike previous precious metals rallies, typically driven by a single catalyst, 2026 features simultaneous stress points across multiple regions. In the Middle East, Israel's June 2025 strikes on Iran's nuclear program triggered retaliation threats, while the Trump administration maintains a "locked and loaded" posture that sent metals prices surging in January.

The capture of Venezuelan President Maduro by U.S. forces sparked a nearly 3% single-session gold rally.

US-China tensions remain elevated despite an October 2025 trade truce that reduced tariffs from a peak of 145% to 30%. That fragile détente faces immediate pressure: Trump's January 2026 threat of 25% tariffs on countries trading with Iran directly imperils the agreement, given that majority of Iranian oil exports flow to China, settled entirely in yuan.

Europe enters 2026 in what Eurasia Group calls a state of "paralysis at best, destabilization at worst."

Many European countries have seen increased government stability risk since 2020. France, Germany, and the UK each face weak governments under siege from populist movements, while the continent's defense readiness faces its sternest test since the Soviet collapse.

Macro conditions favor precious metals

The macroeconomic backdrop could hardly be more favorable for gold and silver. U.S. inflation remains stubbornly above target at 2.7%, while the Federal Reserve has paused rate cuts at 3.50-3.75% after reducing rates by 175 basis points from 2024 peaks.

America's fiscal trajectory has deteriorated dramatically. National debt has reached $38 trillion, representing 121% of GDP. Annual interest payments now exceed $1 trillion, more than Medicare or defense spending individually, and Moody's stripped the U.S. of its last AAA credit rating in May 2025, the first downgrade since 1917.

For investors seeking protection from currency debasement and fiscal instability, gold's appeal as a non-printable asset has rarely been stronger.

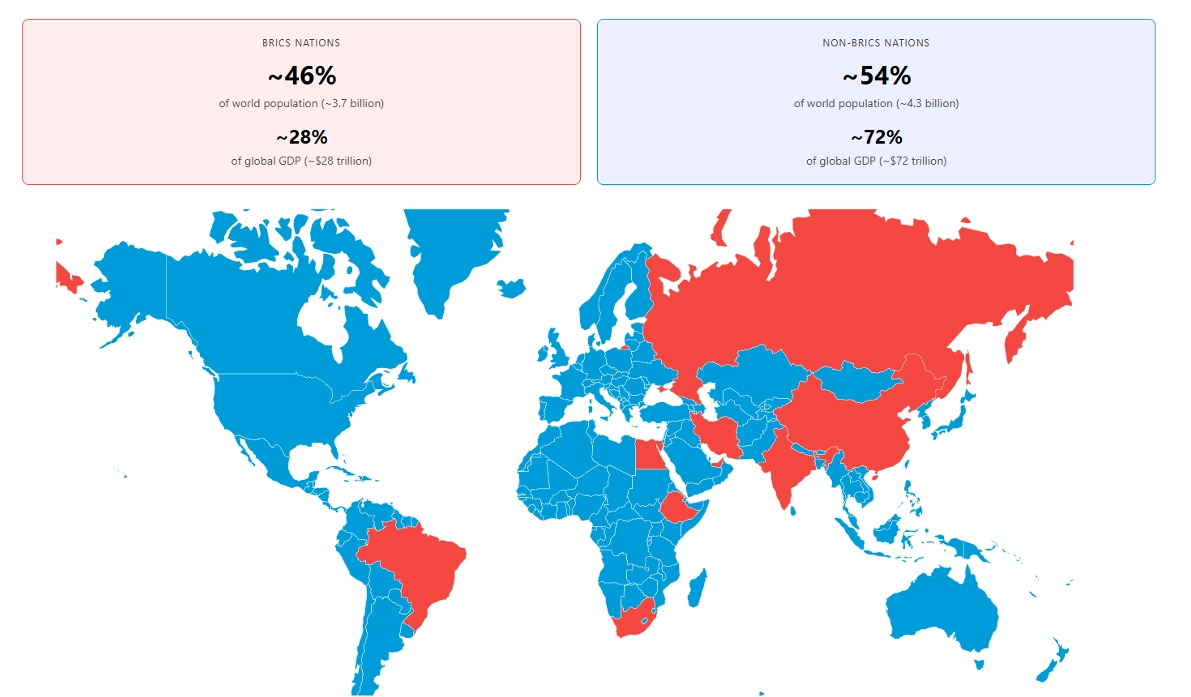

De-dollarization efforts, while gradual, are accelerating. BRICS nations now represent 46% of the world population and 28% of global GDP, with combined gold reserves exceeding 6,000 tonnes.

The bloc has launched a gold-backed currency initiative composed of 40% physical gold and 60% member currencies, while Russia and China now settle close to 90% of bilateral trade in rubles and yuan. The dollar's share of global reserves has declined from over 70% in 2000 to approximately 59% today.

Silver offers a unique upside through industrial demand

While gold benefits primarily from monetary demand, silver enjoys a dual role as both a precious metal and a critical industrial commodity, at a time when industrial fundamentals have never been stronger.

Total industrial demand hit a record 680.5 million ounces in 2024, comprising 59% of global silver consumption.

The green energy transition is reshaping silver's demand profile dramatically. Solar photovoltaic manufacturing consumed 197 million ounces in 2024, nearly 20% of total global demand and triple the level from 2015.

Each solar panel requires 15-25 grams of silver, and the shift to TOPCon cells uses approximately 50% more silver than previous technology. With the EU targeting 700 GW of solar capacity by 2030 and China accounting for 90% of solar-related silver consumption, this demand appears structural rather than cyclical.

Electric vehicles compound the story. Each EV requires 25-50 grams of silver, 67-79% more than conventional vehicles. Silver in EV is used for battery management systems, power electronics, and charging infrastructure.

Data centers powering artificial intelligence have increased IT capacity 53-fold since 2000, driving additional demand for electronics.

Supply cannot keep pace. Silver mining production peaked at 900 million ounces in 2016 and has declined annually since.

Crucially, 72% of mined silver is byproduct from copper, lead, and zinc operations, limiting supply responsiveness to price signals.

The result: a fifth consecutive annual supply deficit in 2025, with cumulative shortfalls reaching approximately 820 million ounces, equivalent to an entire year of global mine production.

The gold-to-silver ratio, which spiked to 105:1 in April 2025, has compressed dramatically to approximately 57:1, still above the long-term average of 50-60:1, suggesting silver may have further room to outperform.

Historical patterns favor precious metals ownership

History strongly supports precious metals during uncertainty. During the 2008 financial crisis, gold gained 47% while the S&P 500 fell 49%.

From its October 2008 low to the September 2011 peak, gold surged 174%. Silver proved even more explosive, rising approximately 450% from its crisis low to its April 2011 peak of $49.82.

The COVID-19 pandemic repeated this pattern. Gold climbed 25% in 2020, briefly exceeding $2,000 for the first time in August. Silver rallied 146% from its March 2020 low to August highs in under five months.

During the 1970s stagflation, when inflation peaked at 14.5%, gold delivered a staggering 2,300% gain from 1970 to 1980, making it the decade's best-performing asset class.

Major institutions project continued strength

Wall Street consensus points to further gains. J.P. Morgan forecasts gold averaging $5,055 by Q4 2026, with the potential to reach $5,400 by the end of 2027.

Goldman Sachs targets $4,900, while UBS and Bank of America both project $5,000. Yardeni Research, the most bullish major institution, sees $6,000.

Silver forecasts are equally constructive. Citi projects $110 per ounce in the second half of 2026, citing acute physical shortages.

Goldman Sachs calls silver the "primary strategic metal of the green transition," targeting $85-100.

Some independent analysts, including GoldSilver's Alan Hibbard, project $175 or higher.

Investor Takeaway

For investors seeking portfolio insurance against an increasingly uncertain world, the case for precious metals in 2026 is compelling across multiple dimensions.

Central banks are accumulating gold at rates unseen in decades. Geopolitical tensions spanning the Middle East, Asia, and Europe show little sign of resolution.

Fiscal deterioration and stubborn inflation provide macro tailwinds, while de-dollarization trends add structural demand.

Silver's unique position at the intersection of monetary and industrial demand, with solar, EV, and AI sectors driving consumption against declining supply, creates asymmetric upside potential.

A 5-15% allocation to precious metals, as recommended by institutions ranging from the World Gold Council to Morgan Stanley, may provide both crisis protection and meaningful return potential in an environment where traditional safe havens face unprecedented challenges.